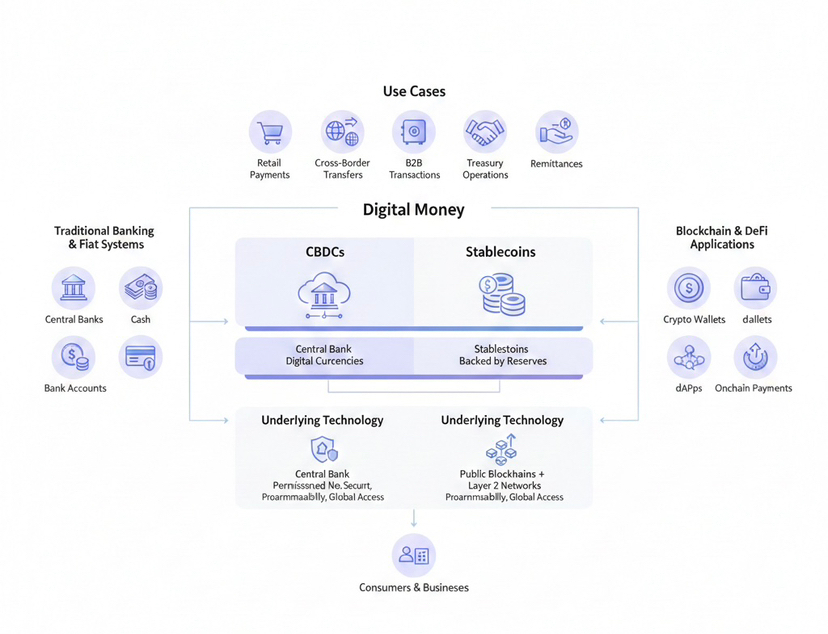

Digital money isnt just about flashy crypto anymore it is going mainstream and two big players are shaping the game CBDCs Central Bank Digital Currencies and stablecoins Both are digital cash but they come from very different worlds Think of CBDCs as the governments digital version of your wallet while stablecoins are private companys flexible fast moving cash

Here is the lowdown

CBDCs are straight from the central bank Stablecoins come from private companies or crypto protocols

CBDCs are backed by state reserves Stablecoins use a mix of collateral code or algorithms

CBDCs focus on policy stability and financial inclusion Stablecoins focus on payments speed and global reach

By the end of this you will know who is who in digital money and why both matter for the future of finance

CBDCs Government Backed Digital Cash

CBDCs are digital money issued directly by a countrys central bank Unlike your bank account this is a liability of the state itself It is like cash but digital with rules baked in

Retail CBDCs are for everyday people buy groceries pay rent get your salary Wallets might have privacy tiers but the central bank still watches the flow

Wholesale CBDCs are for banks and financial institutions Think fast settlement of trades real time gross settlements RTGs and Delivery versus Payment DvP magic

Governments are pursuing CBDCs for faster payments financial inclusion and more control over the economy Plus CBDCs are a hedge against private digital money eating into government control

Real world examples include Bahamas Sand Dollar Nigeria eNaira and China e CNY Some are live some in pilot but the trend is clear governments are waking up to digital cash

Stablecoins Private Digital Money

Stablecoins are crypto tokens pegged to a stable value dollars euros gold or even algorithms Their goal Keep value steady while being fast global and programmable

Fiat backed stablecoins include USDT and USDC pegged 1 to 1 to dollars

Commodity backed stablecoins are backed by gold or other assets like PAXG and XAUT

Crypto backed stablecoins are over collateralized with volatile crypto like USDS and LUSD

Algorithmic stablecoins use code to manage supply Terra UST failed spectacularly

Hybrid and yield bearing stablecoins combine reserves with smart contracts sometimes generating yield like FRAX or Ondo USDY

Stablecoins are already huge In 2024 transfers hit 27.6 trillion dollars beating Visa and Mastercard combined They power cross border payments remittances and treasury operations for businesses

CBDCs vs Stablecoins Head to Head

Governance CBDCs are controlled by the central bank with regulated intermediaries Stablecoins are managed by private issuers or decentralized protocols

Legal Status CBDCs are legal tender Stablecoins are not legal tender they are treated as regulated assets

Backing CBDCs are backed by sovereign reserves Stablecoins are backed by fiat crypto commodities or algorithms

Privacy CBDCs offer tiered privacy with government oversight Stablecoins run on public blockchains some with optional privacy tech

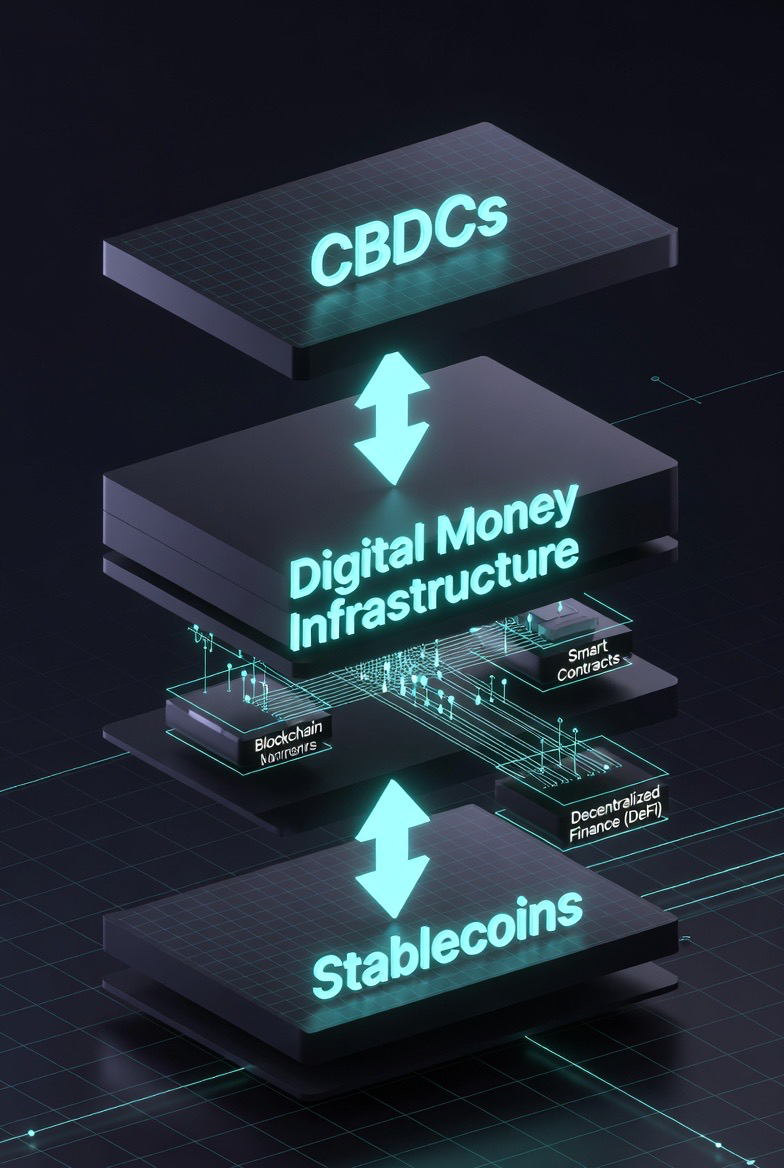

Technology CBDCs use permissioned centralized networks Stablecoins run on public blockchains Layer 2 networks or hybrid systems

Policy Role CBDCs integrate with monetary policy Stablecoins are market driven with no policy control

Resilience CBDCs can be vulnerable to single point of failure Stablecoins use multi chain redundancy but issuer risk remains

Bottom line CBDCs offer stability oversight and policy tools Stablecoins offer speed flexibility and global reach but with higher risk

Risks and Challenges

CBDC risks include privacy erosion because the central bank can see your transactions potential government overreach programmable money tech vulnerabilities downtime or hacks could hit everyone and disintermediation reducing bank lending

Stablecoin risks include depegging if reserves fail transparency issues if proof of reserves is unclear regulatory uncertainty algorithmic failures Terra UST taught a hard lesson and concentration risks relying heavily on one issuer or blockchain

Global Implications

Stablecoins mostly reinforce the US dollar while CBDCs allow countries to assert monetary sovereignty settle payments instantly and reduce reliance on the dollar Cross border CBDC projects like mBridge show the potential for real time foreign exchange fewer intermediaries and geopolitical maneuvering

In the EU authorities are all in on CBDCs plus regulated stablecoins MiCA and the Digital Euro

In the US the focus is stablecoins first CBDCs are debated GENIUS Act 2025 passed but retail CBDCs face political resistance

Who Uses Them

Businesses use stablecoins for global payments and pilot CBDCs for system integration

Financial institutions provide custody settlement and treasury operations

Developers and fintechs build apps integrate wallets and ensure compliance

Policymakers craft tech neutral rules for privacy interoperability and cross border use

Individuals can explore CBDC wallets use transparent stablecoins and balance privacy with convenience

#plasma

The Takeaway

CBDCs and stablecoins show two paths for the future of money

CBDCs are government backed stable policy driven with privacy tradeoffs

Stablecoins are flexible global fast but carry issuer and tech risks

The future of money isnt either or it is a mix Governments and private innovators are shaping a world where you can pay save and move money digitally faster smarter and more connected than ever