@Plasma arrives at a time when stablecoins are still widely misunderstood. They are often described as nothing more than “digital dollars,” as though their relevance begins and ends with price stability. In practice, stablecoins have already evolved into the primary settlement mechanism of a global, informal banking layer. Every day, they transmit more value than many national payment systems—yet they rely on infrastructure that was never optimized for high-volume monetary settlement. Plasma’s ambition is not to become another experimental smart contract ecosystem. Its goal is to function as a place where money reliably settles. That focus sets it apart from nearly everything else in crypto today.

What Plasma understands—and what many Layer-1 networks continue to overlook—is that once money becomes the central use case, predictability, speed, and neutrality outweigh expressiveness. Ethereum prioritized composability and open-ended experimentation, and that design choice paid off enormously. But it also transformed the base layer into a perpetual bidding war for block space, where stablecoin users effectively fund speculative activity they have no interest in. Plasma takes a different stance: monetary transfers should not have to compete with NFTs, liquidations, or meme trades. They belong on infrastructure that treats settlement as the primary economic action, not as collateral damage.

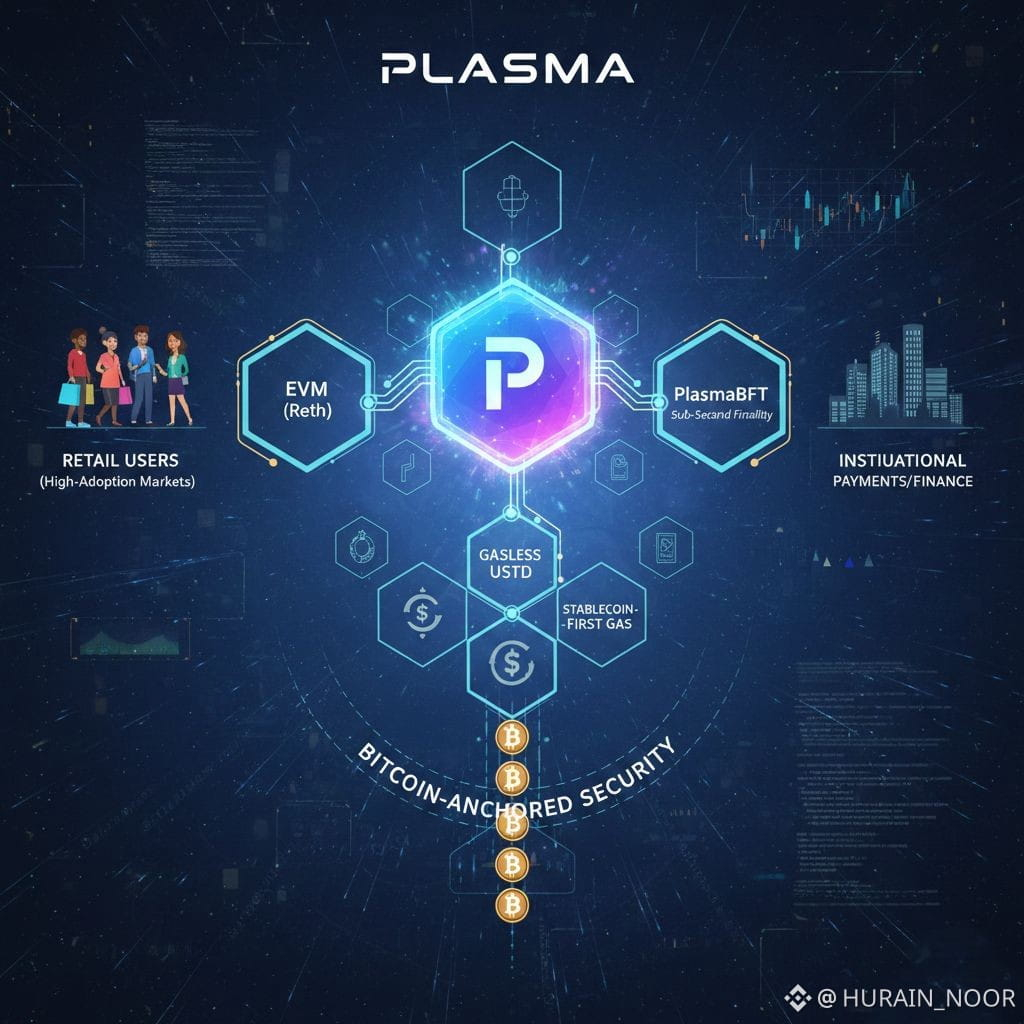

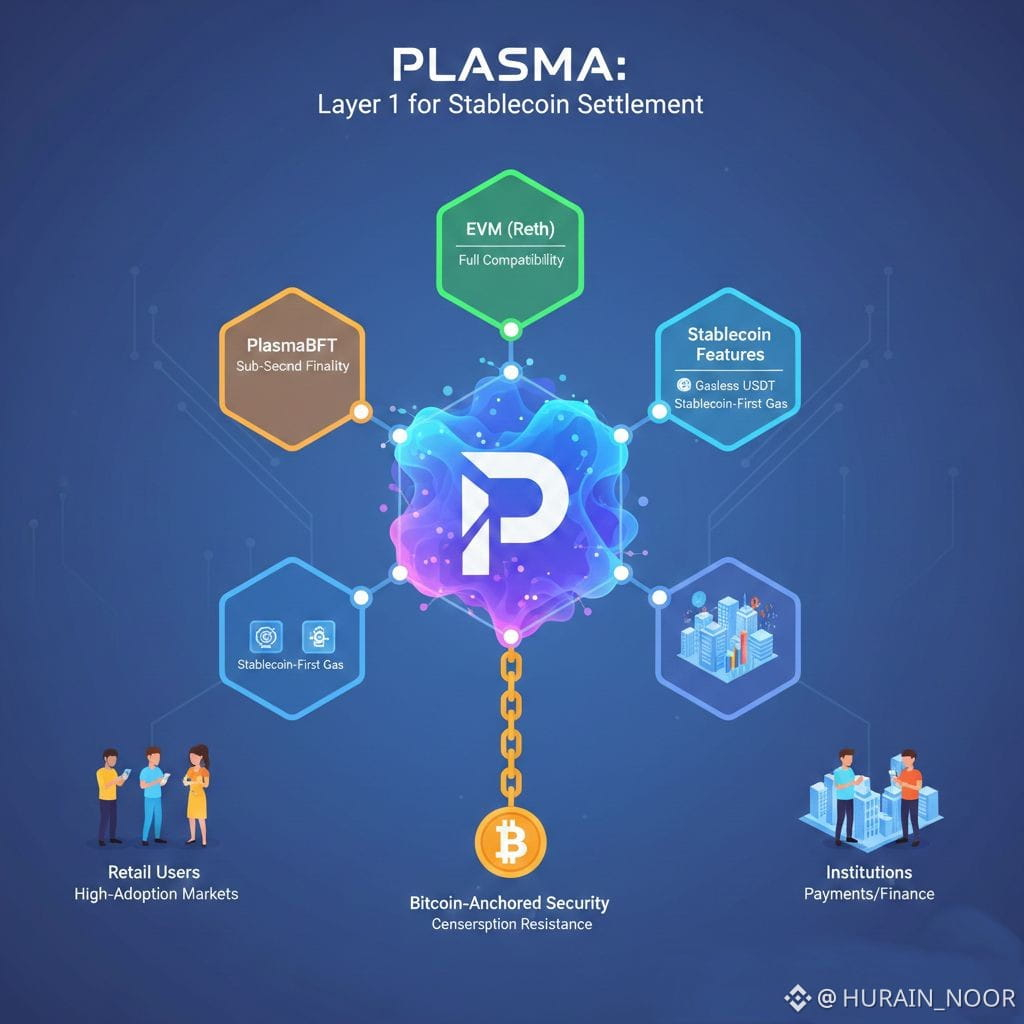

Perhaps the most overlooked aspect of Plasma’s design is not performance or EVM support, but its commitment to deterministic finality. Financial markets value certainty far more than abstract decentralization metrics. A transaction that is “almost final” after half a minute is insufficient for payroll processing, merchant payments, or treasury operations. Plasma is built around the idea that once a transaction is observed, it is complete—no reorgs, no probabilistic guarantees, no waiting for confirmations. This changes incentives and behavior. Institutions can shorten reconciliation cycles, merchants can deliver goods immediately, and stablecoins begin to function like real operating cash instead of speculative instruments.

Finality also transforms how risk is accounted for. On probabilistic chains, uncertainty lives in mempools and block ordering. Advanced traders monetize that ambiguity through MEV, while everyday users absorb the cost through slippage and delayed execution. By compressing uncertainty close to zero, Plasma doesn’t remove extraction entirely, but it relocates it. Over time, on-chain data would likely show more uniform fees, consistent confirmation times, and a meaningful decline in sandwich attacks around basic transfers. This isn’t a moral shift—it’s an economic optimization.

Gasless stablecoin transfers are often dismissed as superficial marketing, but that criticism ignores their broader implications. Eliminating gas from the user experience doesn’t just smooth onboarding; it reshapes wallet design, application logic, and fraud detection systems. When users no longer need to maintain volatile assets just to move money, balances stabilize instead of constantly cycling to pay fees. That stability improves behavioral analysis and makes abnormal activity easier to detect. From a data perspective, transaction intent becomes clearer once gas management noise disappears. These benefits only become obvious when observed across large datasets over long periods.

Plasma’s reliance on paymasters is similarly underestimated. Sponsored transactions introduce a new participant into the economic model: actors who subsidize usage in exchange for scale, insight, or strategic leverage. This mirrors how legacy payment networks function—users rarely see interchange fees directly; they are absorbed into the system. Plasma simply expresses that logic on-chain. Over time, this could lead to competition among sponsors, targeted fee subsidies, and conditional sponsorship tied to identity or behavior. This is not performative decentralization—it is a realistic translation of payment economics into crypto-native form.

Anchoring Plasma’s state to Bitcoin is often misinterpreted as a branding exercise. In reality, it is about long-term neutrality. Bitcoin’s ledger is not only secure; it is politically resistant. By committing Plasma’s state to Bitcoin at intervals, ultimate arbitration is pushed to a system that no single regulator or alliance can easily control. This matters far more for stablecoins than for speculative assets. If stablecoins are to support global trade, remittances, and institutional treasury flows, their settlement foundation must remain credible across decades, not just bull markets.

This anchoring also creates an important asymmetry. Plasma can operate at high speed precisely because it does not attempt to internalize every security function. Instead, it delegates final dispute resolution to a slower but more immutable layer. This mirrors traditional finance, where rapid clearing systems are ultimately backed by slower legal processes. In Plasma’s case, that backstop is cryptographic rather than judicial. On-chain data would reflect this separation as high transaction throughput on Plasma alongside less frequent Bitcoin checkpoints—a feature, not a flaw.

Plasma’s EVM compatibility is less about attracting developers and more about preserving liquidity flow. Stablecoins exist within a broader ecosystem of lending platforms, derivatives, AMMs, and structured financial products. Execution compatibility with Ethereum allows capital to move without rewriting the logic that manages risk. That continuity is critical for institutional adoption. Serious capital doesn’t migrate to environments that require entirely new tooling or assumptions. Plasma leverages existing inertia rather than fighting it.

At the same time, optimizing the base layer for settlement subtly reshapes DeFi dynamics. Lending markets would experience less violent liquidation behavior because repayments and price updates finalize faster. AMMs would face reduced toxic flow around block boundaries as deterministic finality compresses arbitrage windows. Oracle design would shift as well—latency becomes the dominant concern rather than reorg protection. Over time, this would be visible in higher update frequencies and lower variance across oracle feeds.

Even GameFi, often dismissed in infrastructure discussions, benefits from these design choices. Many on-chain games fail because latency and transaction costs disrupt immersion. When every action feels like a financial decision, engagement drops. Instant, gasless stablecoin transfers allow in-game economies to operate in stable units without value leaking to infrastructure fees. The result is healthier internal circulation of money and less extraction by the underlying chain—closer to a functioning economy than a novelty.

Plasma also sits outside the usual Layer-1 versus Layer-2 framing. Rollups inherit the congestion dynamics of their settlement layer, even when execution is compressed. Plasma avoids this by redefining the base layer’s purpose. It is not positioning itself as a general-purpose world computer, but as a global clearing system. That clarity enables trade-offs—such as prioritizing settlement over maximal composability—that rollups cannot easily make. In time, it would not be surprising to see rollups settling to Plasma instead of Ethereum, driven by economic alignment rather than decentralization rhetoric.

Another underexplored implication is how Plasma could change on-chain analytics itself. Today, stablecoin activity is scattered across chains with inconsistent fee structures and settlement rules, forcing analysts to normalize data before drawing conclusions. A chain purpose-built for stablecoin settlement would generate cleaner signals: fewer dust transfers, more consistent transaction sizes, and timing patterns aligned with real business cycles. This would enable macro-level insights—such as regional payment stress or demand shifts—using on-chain data alone.

Early capital movements already suggest this direction. Liquidity is flowing less toward maximal yield and more toward minimal operational risk. Treasury teams prioritize reliability, predictability, and exit certainty. Plasma’s architecture directly addresses those concerns. Over time, balance data would likely show an initial incentive-driven inflow followed by more persistent holdings tied to operational use. That second phase matters most. Incentives disappear; workflows endure.

None of this is risk-free. Mispriced sponsorship can be exploited. Validator sets tuned for speed must guard against concentration. Regulatory pressure on stablecoin issuers could spill over into usage patterns. But these risks are not unique—they are simply more visible because Plasma is explicit about its objectives. It does not pretend to optimize for everything while delivering little of what money actually requires.

If Plasma succeeds, its impact will not be measured by total value locked or the number of deployed contracts. It will be measured by its ordinariness. When infrastructure works, it fades into the background. The most meaningful chart will not track token prices, but transaction costs flattening toward zero as volume steadily rises. That is what mature financial plumbing looks like.

Plasma is not attempting to replace Ethereum, Bitcoin, or traditional finance. It aims to sit between them and reduce friction at their boundaries. In doing so, it forces a long-avoided question back into focus: are blockchains primarily tools for asset speculation, or systems for moving money? Plasma’s answer is unambiguous—and whether the market agrees may shape crypto’s next decade more than any narrative cycle ever will.