Navigating the Strategic Convergence of Macro Policy, Corporate Shifts, and Bitcoin’s Structural Divergence

1. Introduction: The Eye of the Storm in Global Markets

Global financial markets are currently navigating a "perfect storm," where the superficial calm of price action masks a deeper, more turbulent regime shift. While indices like the Nasdaq and assets like Bitcoin appear to be in the eye of a hurricane, their volatility is a symptom of a significant transition from expansion to targeted liquidity withdrawal. To the untrained eye, the current "loss of momentum" looks like the beginning of a terminal decline; however, a macro strategist views this as a "volatility event" rather than a trend reversal.

Critical indicators of system health, such as the MOVE Index (bond volatility) and the HYG (High-Yield Bond ETF), remain remarkably stable, suggesting that despite the localized turbulence, there is no structural damage to the financial plumbing. We are in a period of "forced digestion," where the underlying fiscal mechanics are challenging institutional capacity, but not yet breaking it.

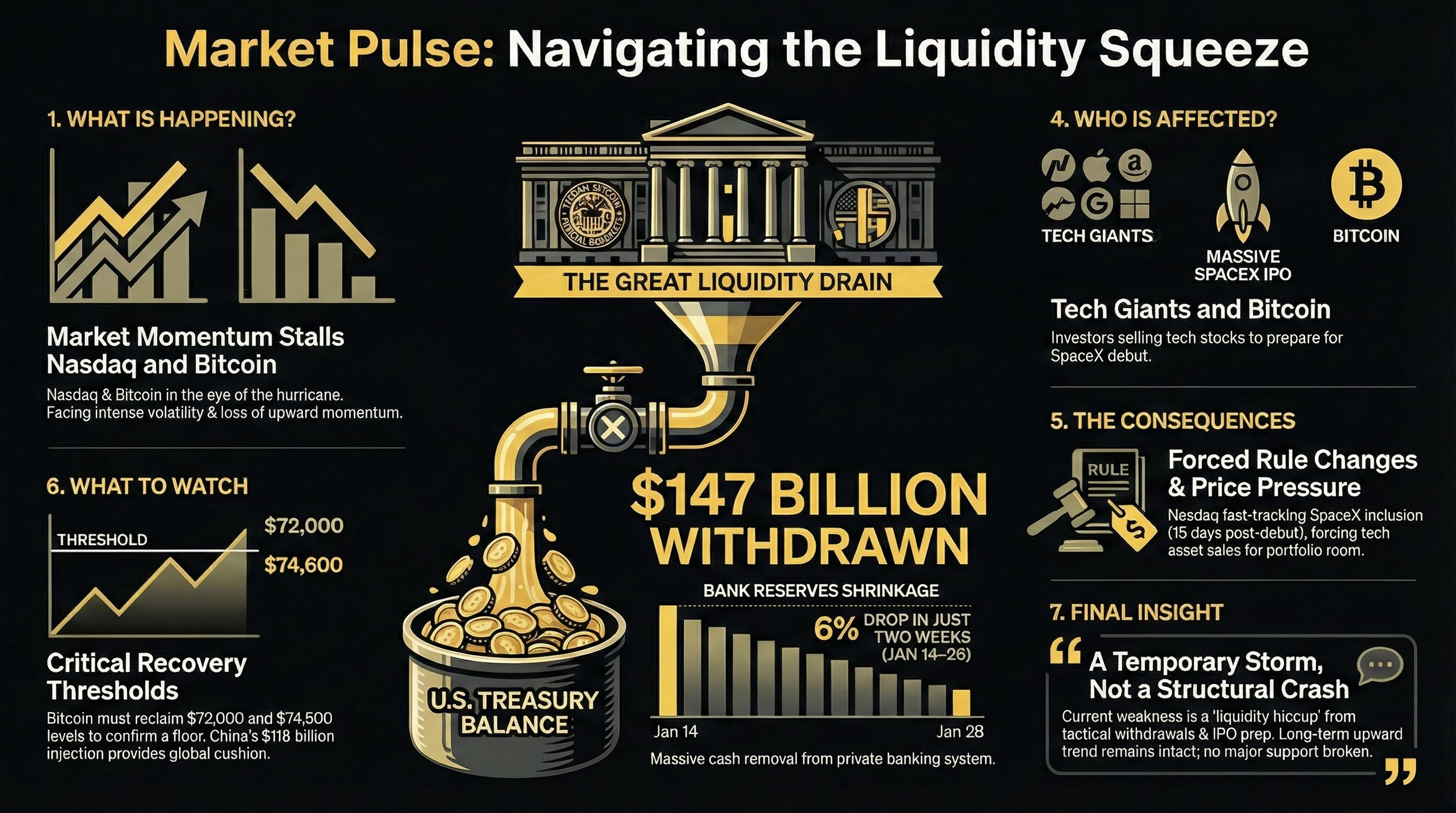

2. Sterilizing the System: The $147 Billion Vanishing Act

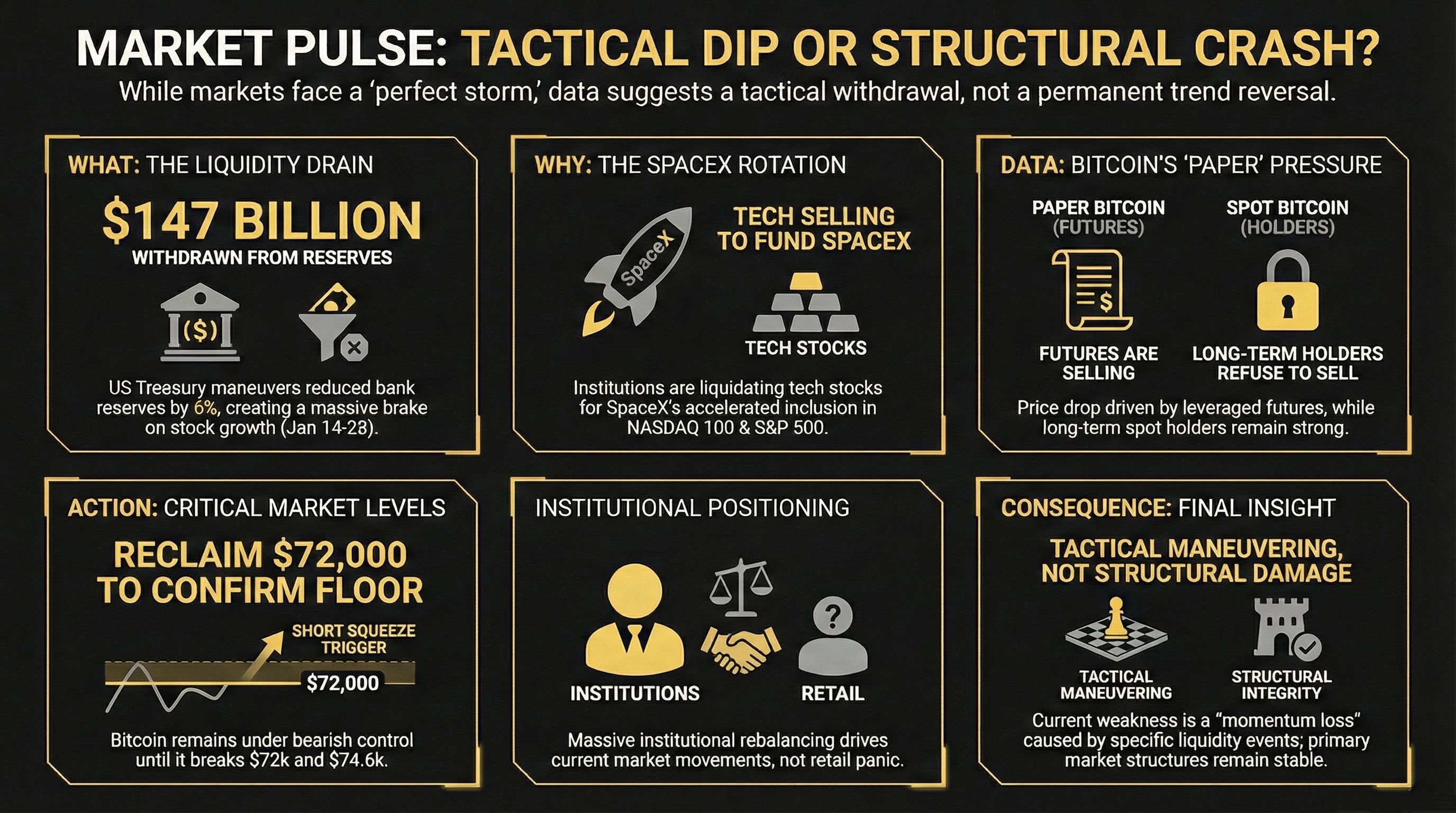

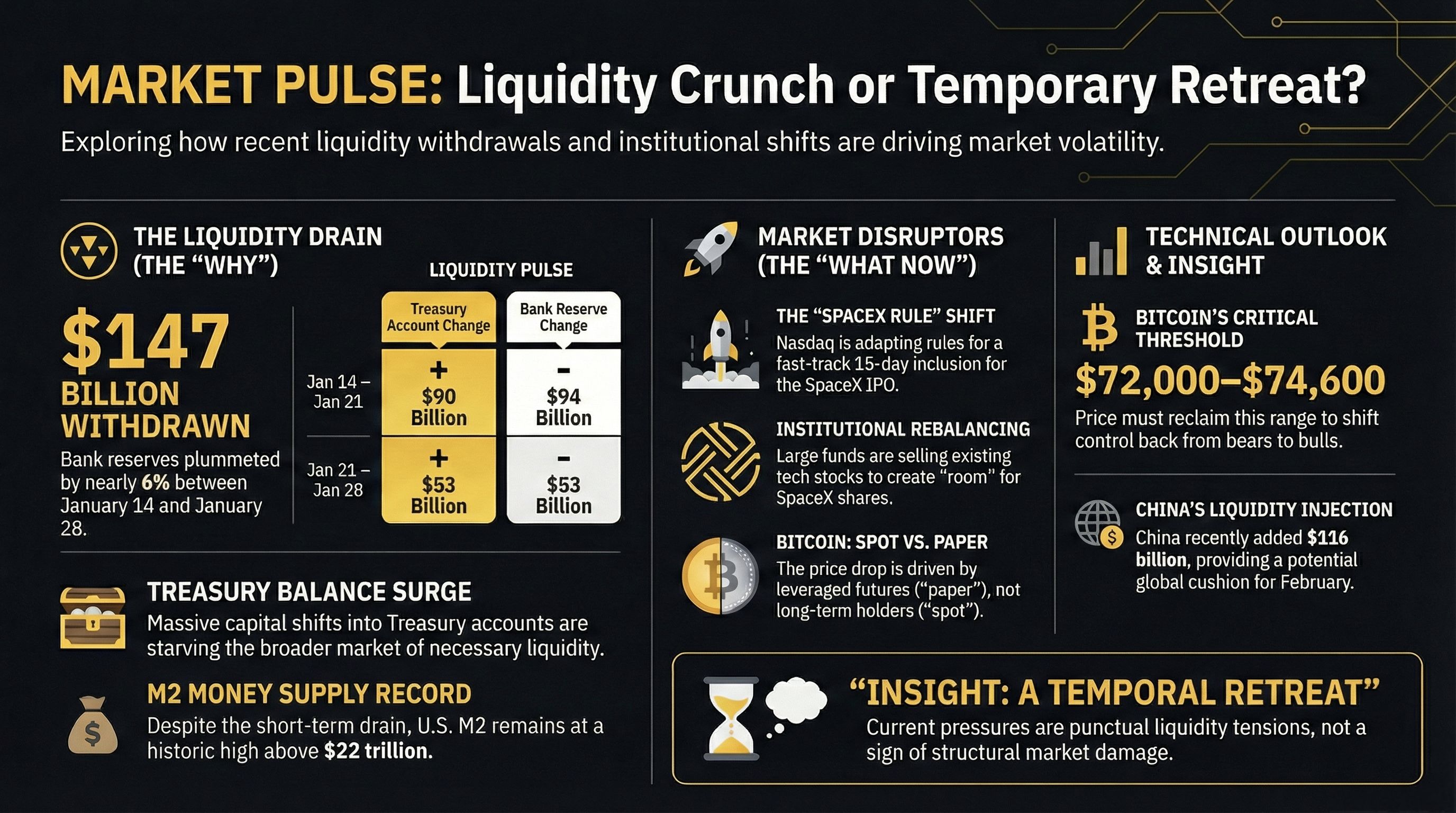

In the current macro environment, price movements are often secondary to the movement of cash between Janet Yellen’s Treasury and the Federal Reserve. The Treasury’s aggressive sterilization of reserves has effectively bottlenecked institutional momentum. When the Treasury expands its account balance at the Fed (the TGA), it acts as a liquidity vacuum, pulling cash directly out of the private banking system.

The Mechanics of the Reserve Contraction

Between January 14th and January 28th, the market underwent a massive, mechanical liquidity drain. This was not a fundamental shift in economic outlook, but a direct consequence of the Treasury’s cash management strategy.

The $147 Billion Drain (Jan 14 – Jan 28):

The TGA Vacuum: The Treasury’s account at the Fed saw an increase of $53,000 million in the final week of January alone.

Direct Sterilization: This move was mirrored by a corresponding $53,000 million contraction in bank reserves during that same window.

The Fortnightly Impact: Over the full 14-day period, total bank reserves plummeted by $147,000 million, representing a staggering 6% reduction in total system liquidity.

This withdrawal forces a pause in equity rallies. Institutions cannot sustain upward momentum when the very "fuel" for their trades is being siphoned back into the Treasury’s coffers.

3. The Dragon’s Buffer: China’s Role as a Global Liquidity Stabilizer

While the United States pursues a policy of withdrawal, the People’s Bank of China (PBoC) is acting as the global counterweight. This creates a strategic tug-of-war for risk assets, where Chinese injections provide a buffer against American tightening.

90-Day Lifelines and the 6-Month Outlook

During the Lunar New Year period, the PBoC injected $116 billion into the system via 90-day instruments. A granular look at these numbers reveals that 100 billion consisted of rollovers, leaving 16 billion in "new" liquidity. While the pace of injection has slowed, it remains a critical intervention to prevent a credit crunch.

The strategic outlook for February suggests a more aggressive expansion from the PBoC:

6-Month Repo Injections: Anticipated after the holiday season to provide medium-term stability.

Long-Term Bond Purchases: A move designed to inject a substantial volume of cash directly into the economy, countering the U.S. liquidity vacuum.

4. The SpaceX Catalyst: Index Engineering and Institutional Rebalancing

The impending SpaceX public offering is more than a landmark IPO; it is an exercise in index engineering that is distorting current equity prices. With a rumored valuation of $420 per share, SpaceX’s entry necessitates a major overhaul of the Nasdaq 100 and S&P 500.

The Breadth Divergence and "Fast Entry" Rules

The "Fast Entry" rule—allowing inclusion just 15 days after debut—is forcing a mechanical sell-off in the technology sector. The "smoking gun" for this theory is found in the breadth of the market: recently, 70% of S&P 500 stocks closed up, while the index itself (weighted heavily by tech) closed down.

Magnificent 7 Pressure: The "MS" ETF (tracking the Magnificent 7) is currently locked in a "sideways triangle," reflecting consolidation rather than a crash.

Index Arbitrage: Institutional players are liquidating "Magnificent 7" positions to make room for SpaceX’s massive anticipated weighting. This selling isn't a sign of fundamental weakness, but a requirement of index tracking.

5. Bitcoin’s Dual Identity: The Conflict Between "Paper" and "Spot"

Bitcoin is currently trapped in a battle between its "Spot" (physical) market and its "Paper" (derivatives) market. This "synthetic" selling, often manufactured on low weekend volume, is designed to drive prices down for institutional entry.

Negative Gamma and the "Perforated" Floor

The recent price drop was led by leveraged futures and negative gamma in the options market, rather than on-chain selling by long-term "whales." Sophisticated players who missed the initial rally are likely using "Paper" Bitcoin to depress the price, creating liquidity for their "Spot" accumulation.

Critical Technical Thresholds:

$72,000: The immediate hurdle. Bulls must reclaim this level to wrest control back from the derivative-led bears.

$74,600: Previously the "magic line" or miner's floor, this level was perforated (broken) during the recent sell-off. Until this level is reclaimed, the technical setup remains precarious.

However, with the futures market overwhelmingly bearish, the system is primed for a gamma squeeze. A sudden rebound could trigger a cascading short squeeze as leveraged sellers are forced to cover.

6. Conclusion: Strategic Reflection on Market Resilience

The current market environment is a masterclass in "forced digestion." The combination of a $147 billion liquidity drain, the mechanical rebalancing for SpaceX, and the derivative-led volatility in Bitcoin has created a temporary vacuum in momentum.

Yet, the long-term tailwinds remain undeniably bullish. U.S. M2 money supply grew at 4.5% in December, hitting a new record high above $22 trillion. This expansion of the money supply contradicts the narrative of a terminal decline. We are not witnessing a collapse; we are witnessing a tactical repositioning. For the disciplined strategist, the current lack of momentum is not a signal to exit, but the foundation for the next liquidity-driven expansion cycle.