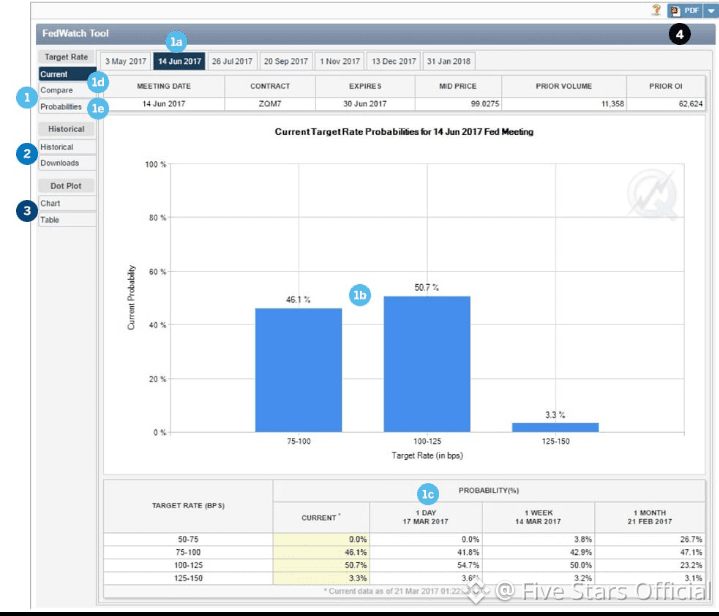

Fed Watch – Today Update:

The FedWatch outlook is signaling a growing shift in market expectations as traders increasingly price in rate cuts later this year. Softer inflation data and cooling labor indicators have strengthened the case that current rates may be restrictive enough, reducing the need for further tightening.

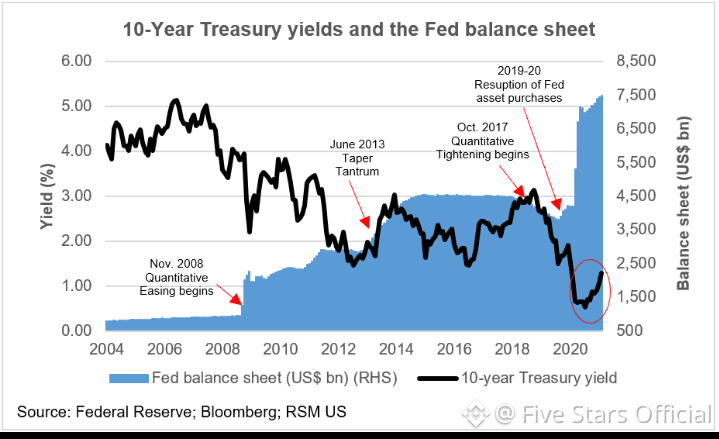

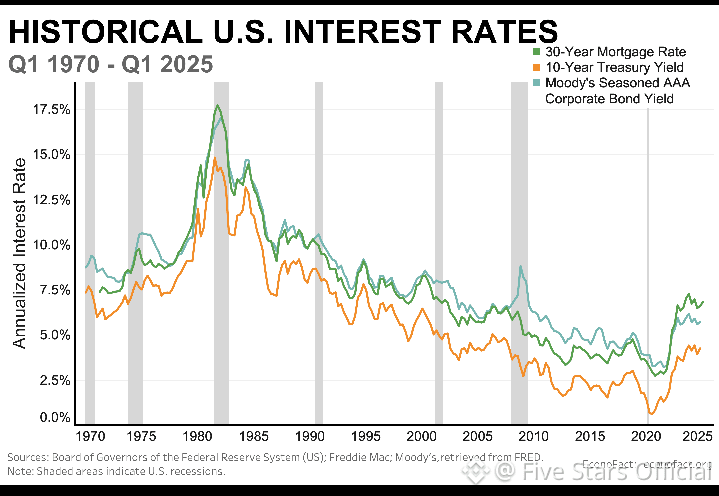

Bond yields remain sensitive to incoming macro data, while equities and risk assets are reacting positively to any sign of a policy pivot. However, the Fed is still walking a tightrope — premature cuts risk reigniting inflation, while staying too tight could slow growth further.

📌 Key takeaway: Markets are betting on easing, but the Fed remains data-dependent. Volatility around CPI, jobs reports, and FOMC meetings is likely to stay elevated.

FedWatch probabilities continue to reflect a clear shift toward monetary easing, with markets increasingly expecting the Fed to begin cutting rates later this year. Cooling inflation, easing consumer demand, and signs of stress in interest-rate-sensitive sectors are strengthening the argument that policy is now sufficiently restrictive.

That said, the Fed remains firmly data-dependent. While headline inflation has slowed, core inflation and wage growth are still being watched closely. Any upside surprise in CPI or jobs data could quickly push rate-cut expectations further out, triggering volatility across equities, bonds, and crypto.

Treasury yields are sending mixed signals — short-term yields remain elevated, while longer maturities suggest growth concerns, reinforcing recession-risk narratives. This tension explains why markets react sharply to every macro release tied to inflation or employment.

📌 Bottom line: FedWatch shows markets leaning dovish, but conviction is fragile. Until the Fed clearly signals a pivot, expect sharp swings around CPI, NFP, and FOMC events — patience and positioning matter more than prediction.