If you’ve been watching WAL and wondering why it can feel “dead” even when the product news keeps coming, I think the market is pricing Walrus like a generic storage token instead of what it actually is: a throughput-and-reliability business where the real choke points are the operators in the middle. Right now WAL is trading around $0.12 with roughly ~$9M in 24h volume and a market cap near ~$190M (about 1.58B circulating, 5B max). That’s a long way from the May 2025 highs people remember, with trackers putting ATH around $0.758, which is basically an ~80%+ drawdown from peak. So the question isn’t “is decentralized storage a thing,” it’s “what part of Walrus actually accrues value, and what has to happen for demand to show up in the token?”

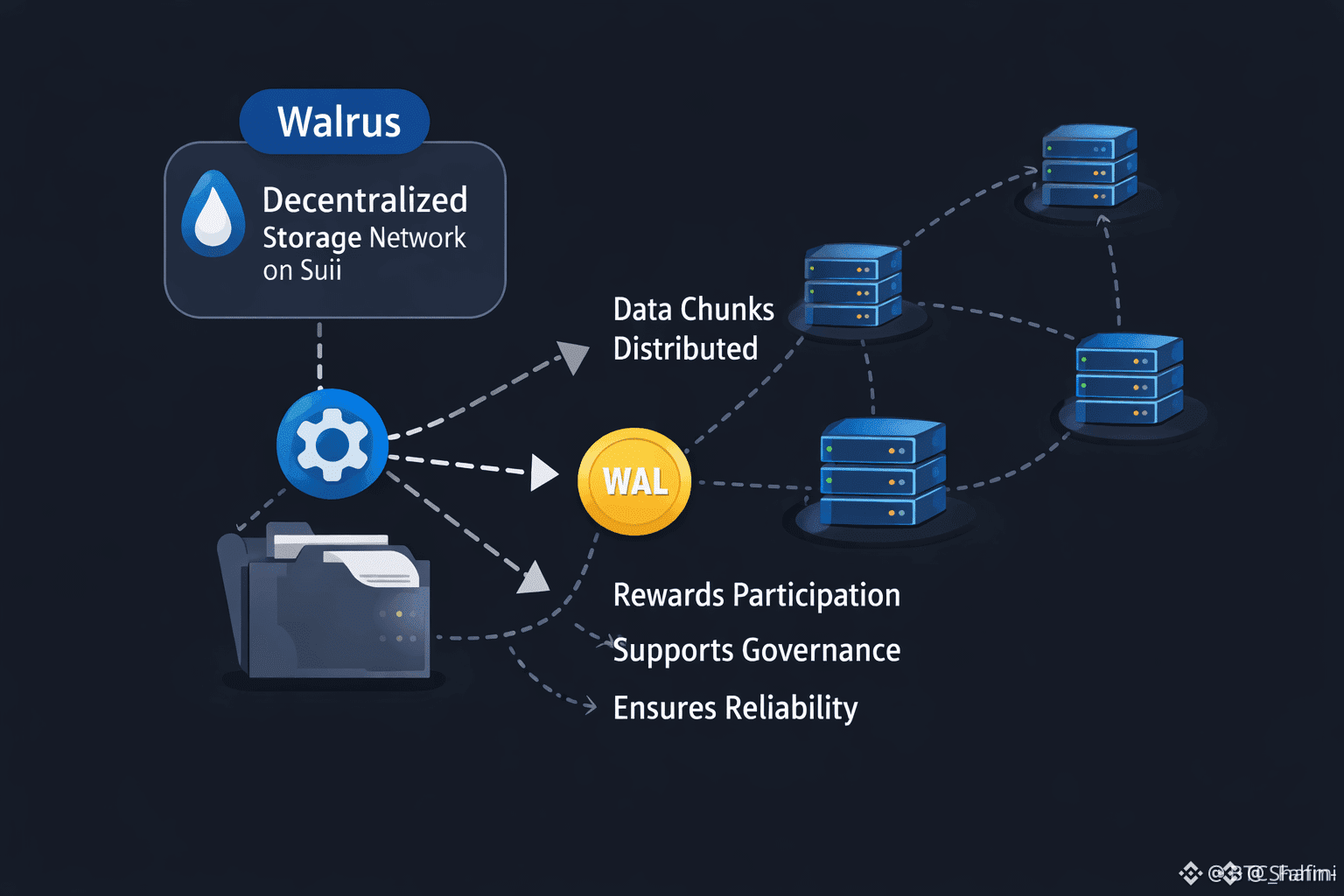

Here’s the moving-parts version that matters for trading. Walrus is built to store big unstructured blobs off-chain, but still make them verifiable and retrievable for onchain apps, with Sui acting as the coordination layer. When you upload data, it doesn’t get copied whole to a bunch of machines. It gets erasure-coded into “slivers,” spread across storage nodes, and the system is designed so the original blob can be reconstructed even if a large chunk of those slivers are missing. Mysten’s original announcement frames this as being able to recover even when up to two-thirds of slivers are missing, while keeping replication overhead closer to cloud-like levels (roughly 4x–5x). If you trade infrastructure tokens, that sentence should jump out. That’s the difference between “we’re decentralized” and “we might actually be cost-competitive enough to be used.”

Now here’s the thing most people gloss over: end users and apps typically aren’t talking to raw storage nodes. They go through publishers and aggregators. The docs are pretty explicit about it. A publisher is the write-side service (it takes your blob, gets it certified, handles the onchain coordination). An aggregator is the read-side service (it serves blobs back, and it can run consistency checks so you’re not being fed garbage). Think of storage nodes as warehouses, publishers as the intake dock, and aggregators as the delivery fleet plus the “did we ship the right box?” verification layer. Traders love to model “network demand,” but in practice, UX and latency live at the aggregator layer. If aggregators are slow, flaky, or overly centralized, the product feels bad even if the underlying coding scheme is great.

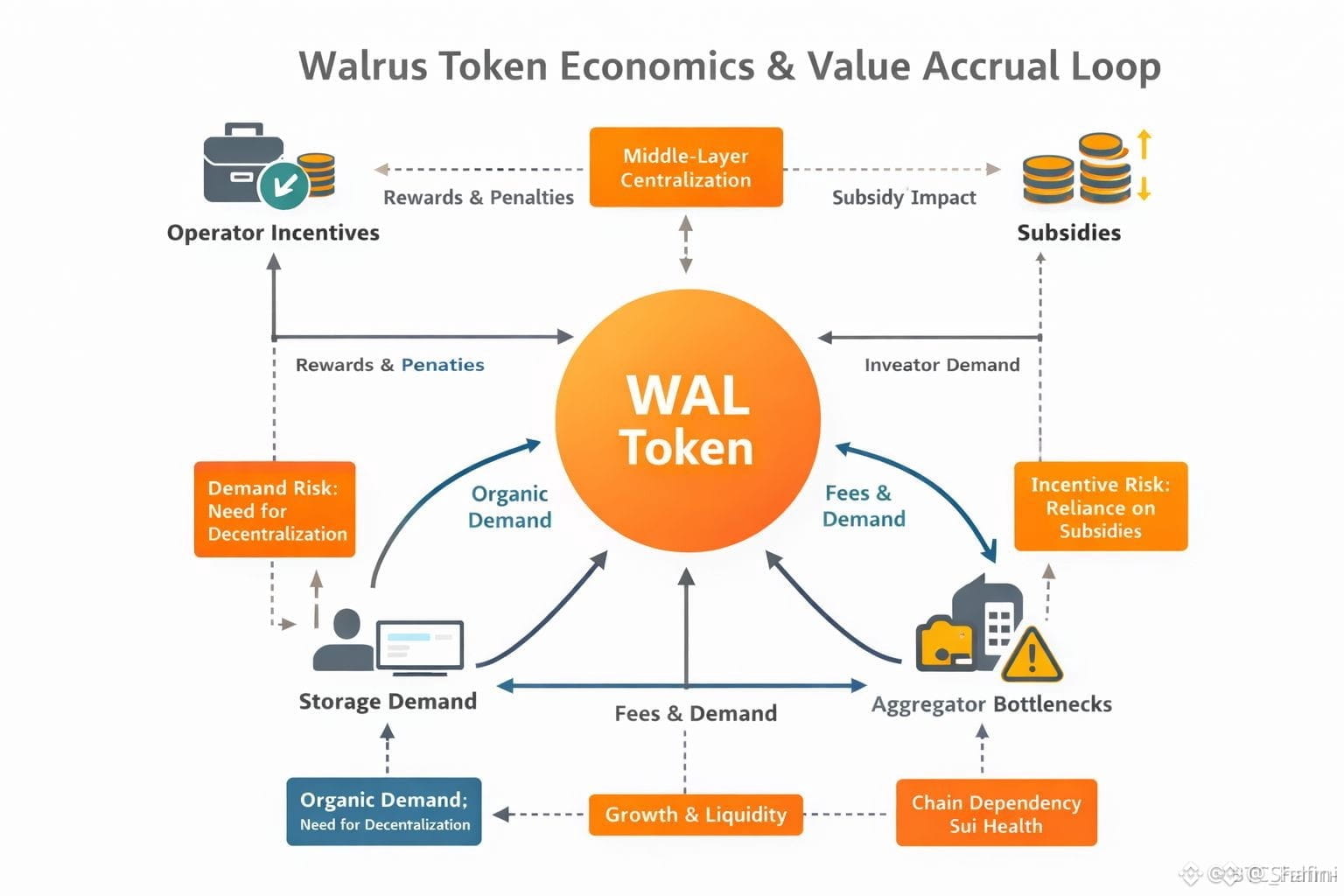

This is why Walrus’s architecture matters for WAL’s economics. Mainnet launched March 27, 2025, and the project’s own launch post ties the system to a proof-of-stake model with rewards and penalties for operators, plus a stated push to subsidize storage prices early to accelerate growth. Translation: in the early innings, usage might be partially “bought” via subsidies, and token emissions and incentive tuning matter as much as raw demand. That’s not good or bad, it’s just the part you have to price. If you’re looking at WAL purely as a bet on “more data onchain,” you’ll miss that the path there is paved with operator incentives, reliability, and actual app distribution.

So what would make me care as a trader? I’d watch for evidence that aggregators are becoming a real competitive surface instead of a thin wrapper. The docs mention public aggregator services and even operator lists that get updated weekly with info like whether an aggregator is functional and whether it’s deployed with caching. That’s quietly important. Caching sounds boring, but it’s basically the difference between “decentralized storage” and “something that behaves like a CDN.” If Walrus starts looking like a programmable CDN for apps that already live on Sui, that’s when WAL stops trading like a forgotten midcap and starts trading like a usage-linked commodity.

Risks are real though, and they’re not just “competition exists.” First, demand risk: storing blobs is only valuable if apps actually need decentralized availability more than they need cheap centralized S3. Second, middle-layer centralization: even if storage nodes are decentralized, a handful of dominant aggregators can become the practical gatekeepers for reads, and that concentrates power and creates outage tail risk. Third, chain dependency: Walrus is presented as chain-agnostic at the app level, but it’s still coordinated via Sui in its design and tooling, so Sui health and Walrus health are correlated in ways the market will notice during stress. Fourth, incentive risk: subsidies can bootstrap growth, but if real willingness-to-pay doesn’t arrive before subsidies fade, you get a usage cliff and the token charts it immediately.

If you want a grounded bull case with numbers, start simple. At ~$0.12 and ~1.58B circulating, you’re around ~$190M market cap. A “boring” upside case is just re-rating back to a fraction of prior hype if usage and reliability metrics trend the right way. Half the old ATH is about $0.38, which would put circulating market cap around ~$600M-ish at today’s circulating supply. That’s not fantasy-land, that’s just “the market believes fees and staking demand can grow.” The real bull case is if Walrus becomes the default blob layer for a set of high-traffic apps (media, AI datasets, onchain websites), because then storage spend becomes recurring and WAL becomes the metered resource that operators secure and users consume. The bear case is simpler: WAL stays a token with decent tech but thin organic demand, aggregators consolidate, subsidies mask reality, and price chops or bleeds while opportunity cost does the damage.

So if you’re looking at this, don’t get hypnotized by “decentralized storage” as a category. Track the parts that turn it into a product. Are aggregators growing in number and quality? Are reads fast and consistent enough that builders stop thinking about storage as a bottleneck? Are storage node incentives stable without constantly turning the subsidy knobs? And is WAL’s liquidity and volume staying healthy enough for real positioning, not just spot tourists? Right now we at least know the token is liquid and actively traded on major venues, with mid-single-digit millions in daily USD volume.

My base take: Walrus is one of the cleaner attempts to make “big data off-chain, verifiable onchain” feel normal for apps, and the storage nodes-to-aggregators pipeline is where that either works or dies. If the middle layer matures, WAL has a path to trade on adoption. If it doesn’t, it’ll keep trading like a concept.

@Walrus 🦭/acc 🦭/acc $WAL #walrus