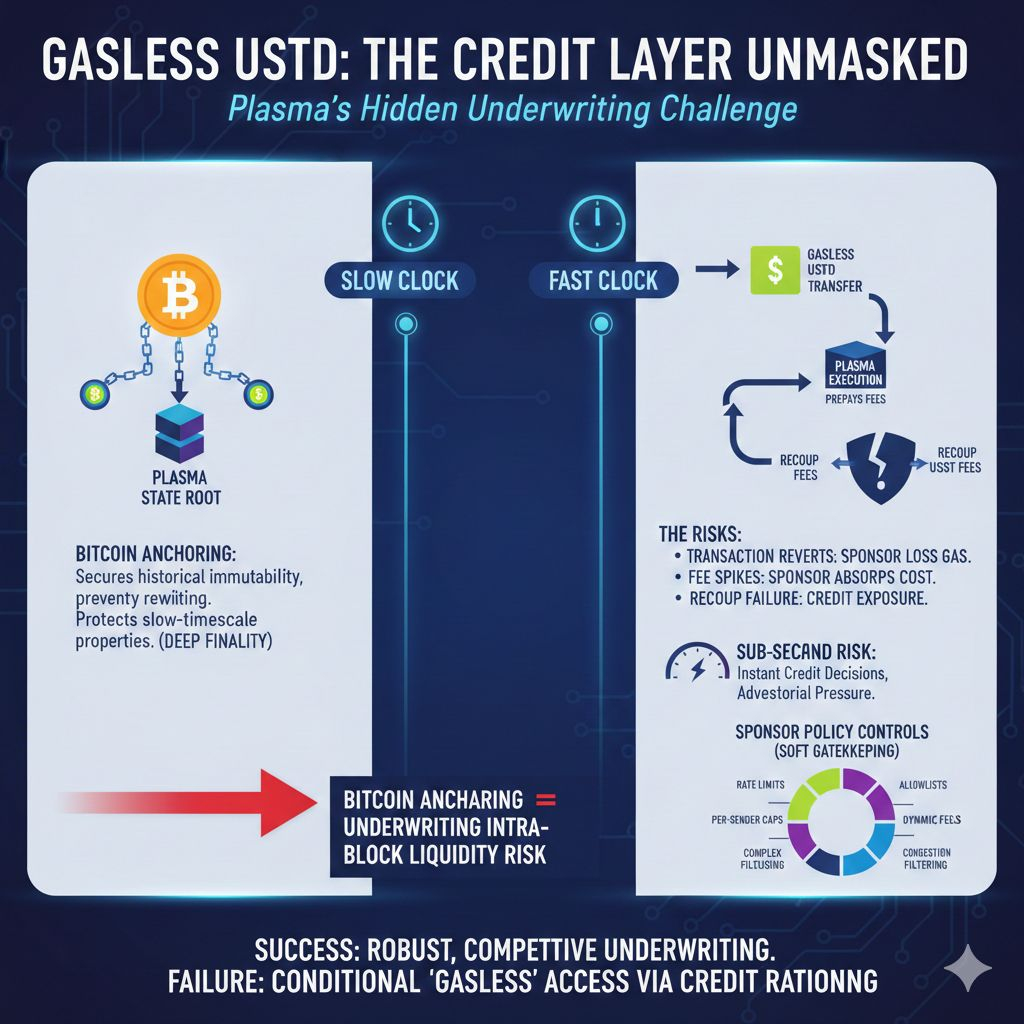

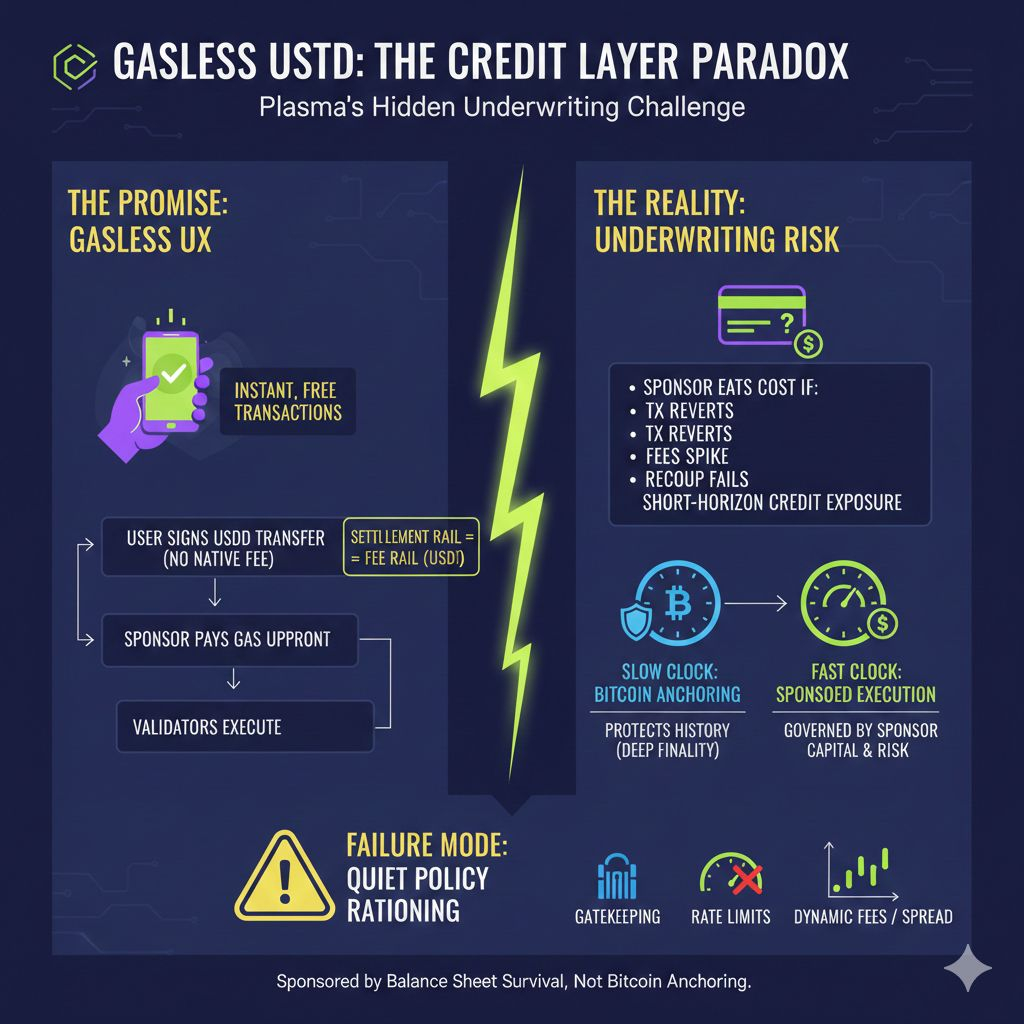

Plasma’s gasless USDT promise only makes sense if the chain quietly inserts a payer-of-last-resort between the user and execution. Validators still need fees and blocks still have scarce space, so “gasless” isn’t the absence of cost, it’s a reassignment of who advances it. On Plasma, stablecoin-first gas sharpens that reality: the same instrument being moved is also the unit used to recover execution costs, which means the settlement rail and the fee rail are no longer independent.

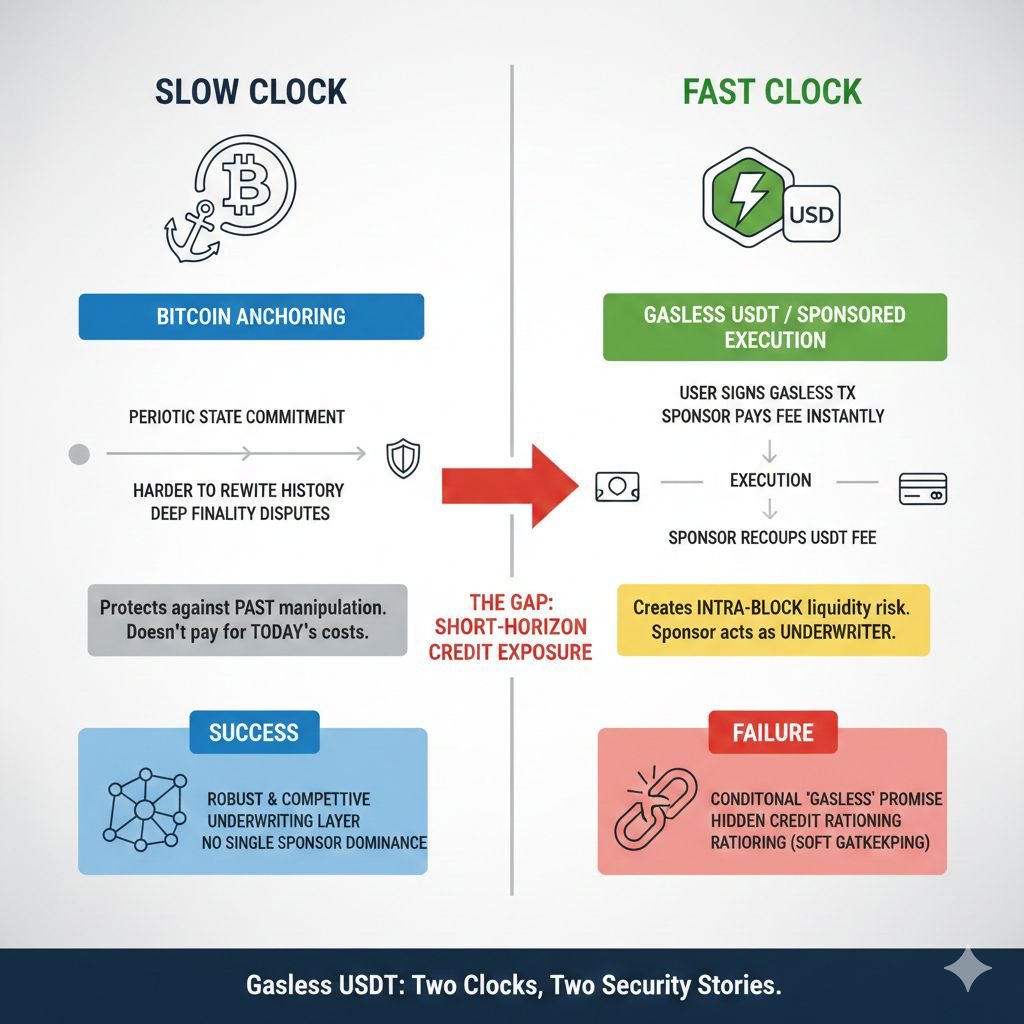

Here’s the minimal flow that turns this into underwriting. A user signs a USDT transfer that carries no native-fee payment. A sponsor layer submits it to Plasma and prepays the execution fee so validators include it immediately. After execution, the sponsor recoups value in USDT, either by taking an explicit fee in USDT, by using a built-in fee abstraction, or by settling against an internal balance it maintains. If the transaction reverts, if fee conditions spike mid-flight, or if the recoup step fails, the sponsor still ate the gas. That gap between “must pay now” and “recover later” is the short-horizon credit exposure hiding under the UX.

Sub-second finality doesn’t reduce that exposure, it concentrates it. When blocks finalize quickly, sponsors have less time to batch, net, or selectively route risk. The sponsor’s real job becomes making instant credit decisions under adversarial pressure: how much gas budget to allocate per block, what per-address or per-session limits to enforce, which transaction shapes to refuse because they are revert-prone, and when to tighten pricing because the chain’s fee conditions are moving faster than a stablecoin fee schedule can safely track. If a sponsor says yes too often, it becomes a loss sponge. If it says no too often, “gasless” devolves into intermittent access.

This is why the Bitcoin-anchored security story can be true and still miss the point users care about. Anchoring can protect a slow-timescale property, like making it harder to rewrite history past a checkpoint by periodically committing a state root to Bitcoin. That’s real, and it can improve neutrality optics by giving Plasma a credible external reference. But it doesn’t pay for today’s sponsored execution, and it doesn’t reimburse the sponsor when an attacker forces expensive work that ends in a revert. Bitcoin can help adjudicate deep-finality disputes after the fact; it cannot underwrite the intrablock liquidity risk that gasless settlement creates by design.

Stablecoin-first gas also creates a coupling that looks tidy until stress shows up. If the sponsor’s recovery is denominated in USDT, then sponsor solvency is tied to USDT liquidity and operational continuity at the exact moment the chain is busy. If USDT routing is impaired, if fee conditions spike, or if the sponsor faces sudden demand from a high-adoption corridor, the sponsor’s balance sheet becomes the throttle. The chain might remain technically live while the practical user experience degrades because the underwriter is rationing capacity.

The most credible failure mode isn’t dramatic collapse; it’s policy. Sponsors will protect themselves with controls that feel like product decisions to users and risk controls to operators. Rate limits, per-sender caps, allowlists for high-confidence flows, dynamic fees that quietly appear as “spread,” selective refusal of complex calls that are more likely to revert, and aggressive filtering during congestion all produce a soft form of gatekeeping even if nobody says the word “censorship.” It’s not ideological. It’s balance-sheet survival.

Plasma-specific security discussion therefore needs two clocks, not one. On the slow clock, Bitcoin anchoring can make history harder to rewrite. On the fast clock, gasless USDT turns the system into a sponsored execution market where the real bottleneck is sponsor capitalization, sponsor competition, and sponsor risk appetite. Users will talk about neutrality while their lived security is determined by whether sponsors keep fronting fees when conditions are worst, not best.

If Plasma succeeds, it won’t be because it made settlement free; it will be because it made the underwriting layer robust and competitive enough that no single sponsor policy becomes the network’s de facto rulebook. If it fails, it will fail quietly: not as a broken chain, but as a chain whose “gasless” promise becomes conditional, where the cost of speed is paid in hidden credit rationing that Bitcoin anchoring, by its nature, cannot meaningfully cover.