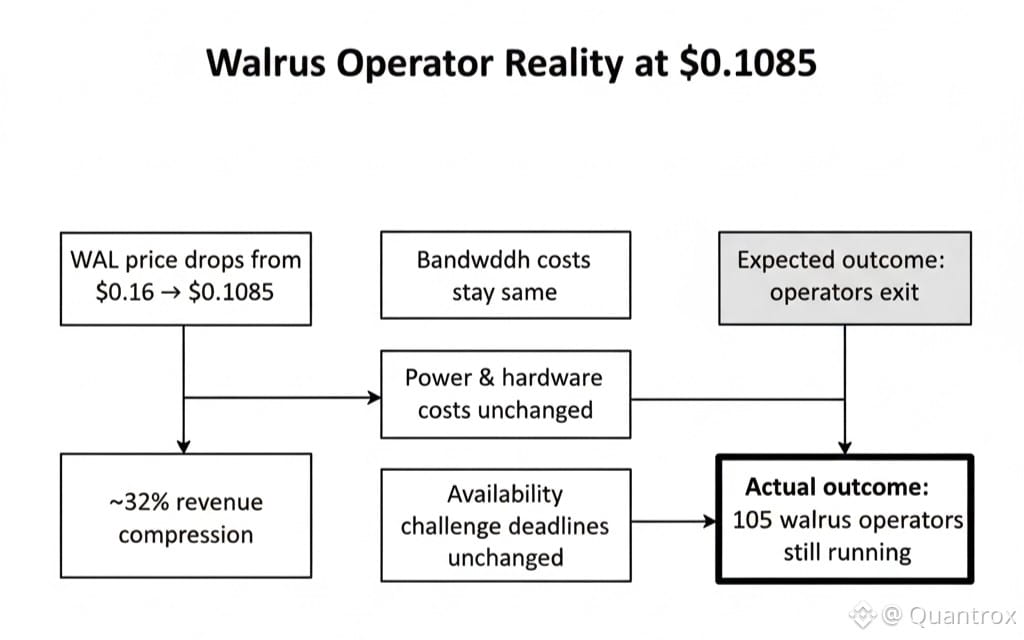

I've been checking the Walrus operator count every few days expecting to see nodes dropping off as the token bleeds lower and it's just... not happening. WAL sits at $0.1085 today with RSI at 23—deep oversold territory that should have people panicking. But those 105 storage nodes that were running when WAL was at $0.14? Still there. Still processing storage. Still serving data. That persistence tells you something about who's actually running Walrus infrastructure.

These aren't yield farmers hoping for quick returns. Those people left months ago.

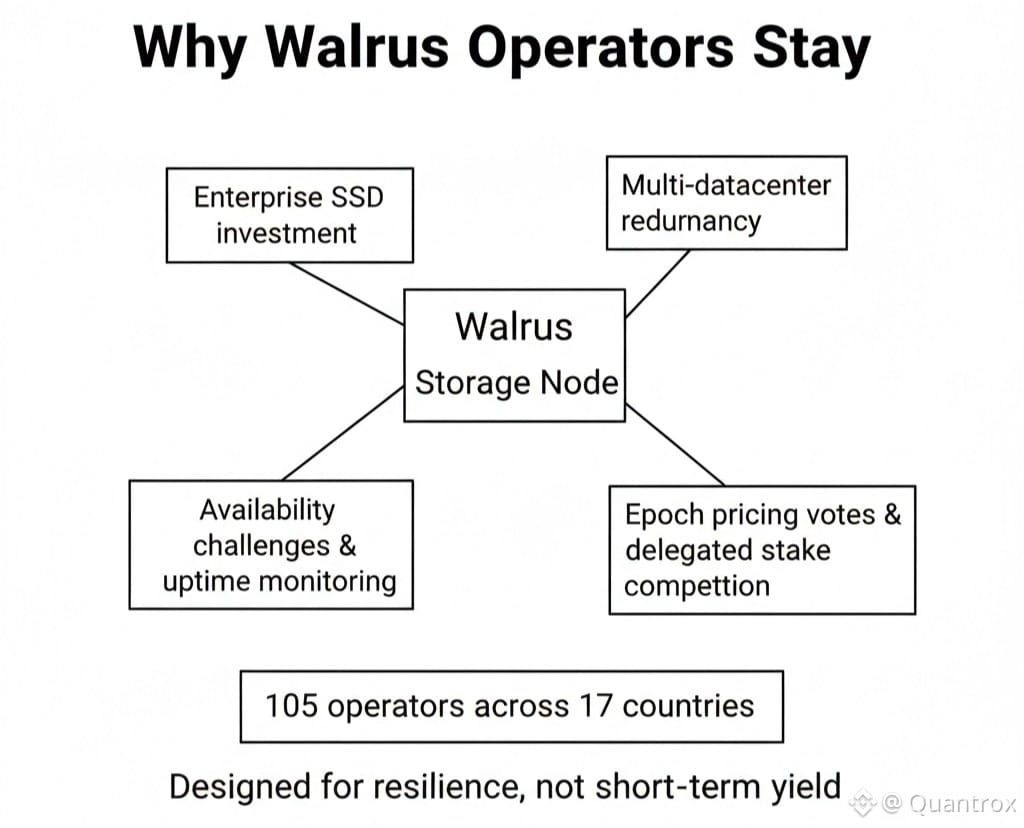

The operators still running Walrus nodes today made infrastructure commitments that don't make sense as short-term plays. You don't buy enterprise SSDs for fast availability challenge responses if you're planning to quit when the token dips. You don't set up redundant systems across multiple datacenters if you're just farming yields. The hardware investment alone means you're in for the medium term whether the token cooperates or not.

Here's what caught my attention. Node count should be declining. Every economic signal says marginal operators should be exiting. Revenue in fiat terms has compressed as WAL fell from $0.16 to $0.1085. That's a 32% revenue cut while operational costs stayed constant. Bandwidth still costs the same. Power consumption didn't drop. Hardware maintenance is still expensive. The math says some operators should have quit by now.

But they haven't. And that's revealing.

Walrus operators stake WAL tokens to participate. They earn storage fees when applications pay for capacity. At $0.1085, those fees are worth less in real money than they were weeks ago. An operator who was breaking even at $0.14 is probably losing money now unless they had substantial margin buffer. Yet the node count stays at 105.

Maybe I'm reading too much into it. Could be that operators are just slow to react. Could be they're waiting for the next epoch boundary to make exit decisions. Could be the losses aren't big enough yet to force anyone out. But there's another explanation that keeps making more sense the longer this persists.

The operators running Walrus infrastructure today believe the network will outlast current token prices. They're not gambling on short-term recovery. They're betting on multi-year adoption curves where storage usage grows enough to justify infrastructure investment regardless of what WAL trades at in January 2026.

That's commitment based on conviction, not speculation based on charts.

Think about what it takes to run a Walrus storage node properly. You need technical expertise to maintain uptime. You need to monitor availability challenges and respond within time limits. You need to understand delegated proof of stake dynamics to attract stake. You need to vote on storage pricing every epoch with some economic rationale. That's work. Real operational work that compounds over time.

The operators still doing that work at $0.1085 aren't just passively holding tokens hoping for recovery. They're actively maintaining infrastructure that serves real applications storing real data. The 333+ terabytes currently on Walrus mainnet didn't get there by accident. Applications uploaded that data because Walrus provided capabilities they needed. And operators keep serving that data because they believe more applications will come.

Walrus processed over 12 terabytes during testnet when there was no revenue at all. Operators ran infrastructure at a loss for months to test the network and establish positioning. That was preparation for mainnet economics that were supposed to work once real fees started flowing. Now mainnet has been live since March 2025, and WAL is testing lows while fees compress. The payback period for testnet investment keeps extending.

But operators are still there. Which means they either miscalculated badly and are trapped by sunk costs, or they calculated correctly for timeframes measured in years rather than months. I'm leaning toward the second explanation. The operators who would have quit at $0.11 probably never joined in the first place. The ones running nodes today are the ones who planned for volatility and priced in the possibility that tokens don't go up.

Here's a concrete reality: geographic distribution costs money. The 105 Walrus operators are spread across 17 countries. That wasn't accident—it was deliberate choice to avoid concentration risks. But coordinating distributed infrastructure is harder and more expensive than just running everything in one AWS region. Operators chose the harder path because they care about resilience and decentralization, not just profit optimization.

That choice reveals values. When operators stick with Walrus at $0.1085, they're reaffirming that the decentralization and resilience mattered more than easy profits. They could have built centralized infrastructure that's cheaper to run. They didn't. They built distributed systems that require more effort and cost more money because the technical properties matter to them.

My gut says the operator count at 105 is actually a feature, not just a number. It's probably close to optimal for current storage demand. More operators would dilute revenue without adding necessary capacity. Fewer operators would risk concentration that undermines decentralization. The count has been stable around this level for months despite token volatility. That suggests Walrus found an equilibrium where the operators who should be there are there, and the ones who shouldn't have already left.

The RSI at 23 screams oversold. Technical indicators say bounce incoming. But operators don't make infrastructure decisions based on RSI. They're looking at storage usage trends, application growth, protocol development roadmap. They're asking whether Walrus becomes essential infrastructure for the Sui ecosystem over the next few years. If yes, operating nodes at temporarily compressed margins makes sense. If no, nothing matters and they should have quit months ago.

The bet they're making is that Walrus crosses the threshold from "interesting experiment" to "necessary infrastructure." Applications building on Sui will need storage. Not all of them will need decentralized storage specifically. But enough will need the properties Walrus offers—Sui integration, programmable access controls, verifiable integrity—that demand grows sustainably over time.

Whether that bet pays off is uncertain. What's clear is that 105 operators are still making that bet at $0.1085. They're putting real money into hardware, bandwidth, and operations every month. They're doing the work to maintain uptime and serve storage requests. They're voting on pricing and competing for delegated stake. That's commitment beyond speculation.

Time will tell whether Walrus operator persistence is wisdom or stubbornness. For now, the infrastructure keeps running while the token tests lows. The applications using Walrus for storage don't care about RSI readings. They care whether data is available when they request it. And the operators are ensuring it is, regardless of what the token does. That's what infrastructure looks like when it's run by people who believe in what they're building, not just what they're trading.