The platform moved 42.8% of total spot volume over the past week but absorbed 79.7% of net selling pressure across major venues, according to market data.

The imbalance raises the question of whether a venue needs to handle “most of the market” to set prices for the whole market.

The answer is no. A venue needs to be where the market most often determines the price.

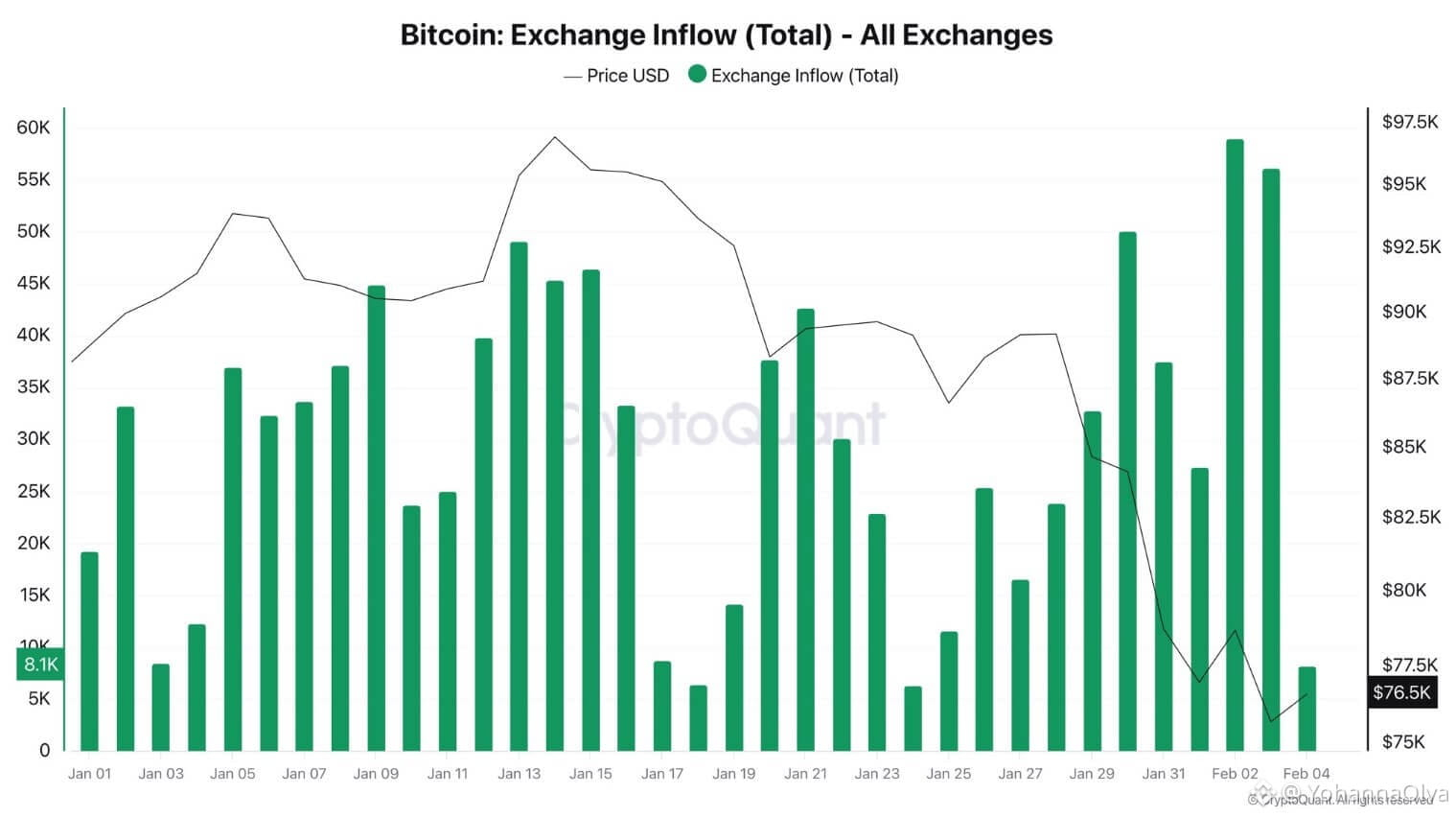

Between Feb. 2 and 3, the platform recorded the largest Bitcoin (BTC) inflows of the year, with roughly 56,000 to 59,000 BTC moving onto the exchange while Bitcoin traded near $74,000, according to public on-chain data.

At current prices, the amount surpasses $4.3 billion in notional terms. Aggregate data shows the platform's 24-hour spot volume runs around $18.5 billion and 251,758 BTC, meaning the inflow represented roughly 22% to 23% of a single day's Bitcoin spot churn on the platform

Deposits raise sell-side optionality by making inventory quickly saleable, but they're not timestamped sell tickets. Analysis of inflows as coins deposited into exchange wallets explicitly cautions that elevated inflows don't always translate into immediate sell-offs.

They can reflect liquidity provisioning for derivatives, collateral movement, or internal settlement. The thesis isn't that the platform “dumped” Bitcoin, but that it became the marginal seller even without controlling most of the market's volume, because it controls the market's most important prints.

Why the marginal seller matters more than the biggest seller

By “net selling pressure,” this means net taker volume: the imbalance between market sells and market buys.

This is often tracked as the cumulative volume delta (CVD), which is a running sum of taker buy volume minus taker sell volume.

Negative CVD indicates more aggressive selling than buying, with market sells lifting bids rather than passive limit orders being filled. It's about who crosses the spread, not just who shows up in headline volume.

The platform sold 3.9 times more Bitcoin than all other major venues combined, according to the data calculation, despite handling less total volume than those venues together. The concentration matters because this platform operates as a structural price-discovery hub.

A recent academic working paper identifies the platform's spot and perpetual futures markets as the primary sources of Bitcoin price discovery, attributing their leadership to lower costs and higher trading volumes.

External research, cited by the platform itself, describes the exchange as offering “deep, resilient liquidity.”

Price discovery doesn't happen everywhere equally. It happens where liquidity is deepest, where derivatives risk unwinds fastest, and where arbitrageurs watch most closely. This platform checks all three boxes.

When perpetual futures risk unwinds, the spot market becomes the hedge leg. That order flow prints the tape, and others reprice around it.

The linkage between leading venues is mechanical.

Arbitrage traders compress dislocations across exchanges by buying where Bitcoin is cheap and selling where it is expensive. When that connectivity works, prices snap together within seconds. When it doesn't, premiums widen and persist.

The cross-venue Bitcoin premium, which tracks the spread between different trading pairs and settlement currencies, is an example.

The premium is not solely attributable to demand, as it reflects differences in plumbing between fiat and stablecoin pairs, funding costs, and transfer frictions.

Yet the premium's behavior reveals how tightly linked venues are. When the premium compresses, arbitrage is re-engaging. When it widens, connectivity is under strain.

How fast Binance-led moves propagate

Cross-venue premium tracking provides a real-time indicator of arbitrage health.

Bitcoin Premium Index characterizes the spread as a connectivity measure rather than a sentiment gauge. A widening premium signals that arbitrage balance sheets are constrained or plumbing has clogged

Three scenarios for what happens next:

When the platform holds the $4.3 billion inflow as inventory at risk, whether it becomes actual selling pressure depends on flows, liquidity, and connectivity.

In the base case, inflows are collateral or positioning, selling pressure fades, and cross-venue premiums compress toward zero. Connectivity recovers.

This scenario becomes more likely if broader flows turn supportive. Spot Bitcoin ETFs saw significant net inflows recently, though they were followed by subsequent outflows the following day.

If institutional demand stabilizes, the platform's marginal selling role could fade.

In the bear case, the platform continues to dominate negative net taker flow, liquidity thins, and premium volatility rises.

Segmentation increases.

The fuel for this scenario exists: reported weekly Bitcoin outflows have been notable. If outflows persist, the platform could remain the marginal seller for weeks.

In the stress case, premiums persist and widen as arbitrage balance sheets get constrained. Plumbing clogs, and price discovery concentrates further.

This echoes the narrative around settlement frictions, funding costs, and transfer constraints. Major drawdowns have been described as deleveraging alongside risk aversion—a regime in which forced selling, not opportunistic buying, sets the price.

A simple calculation illustrates the leverage at play. If even a fraction of the $4.3 billion inflow is aggressively sold while depth is thin, one venue can set the market's marginal price.

The point isn't that #Binance “crashed” Bitcoin, but that when one venue captures most of the negative taker flow, arbitrage forces everyone else to reprice around it.

The story isn't Binance doing something unusual. The story is what happens when the market's marginal seller sits at the venue that also leads price discovery, dominates derivatives, and anchors arbitrage.

ETF flows matter because they change who becomes the marginal seller, such as authorized participants and market makers, and where that selling shows up.

Stablecoin plumbing matters because BTC/USD versus $BTC /USDT isn't a clean spread, but a structural difference in how dollars move

When risk-off hits, deleveraging and liquidity thinning often explain more than any single venue's order flow. However, the mechanics by which that deleveraging translates into price require a marginal seller.

This week, that seller appears to be Binance. Not because it manipulated anything, but because it's where the market goes to find out what Bitcoin costs.