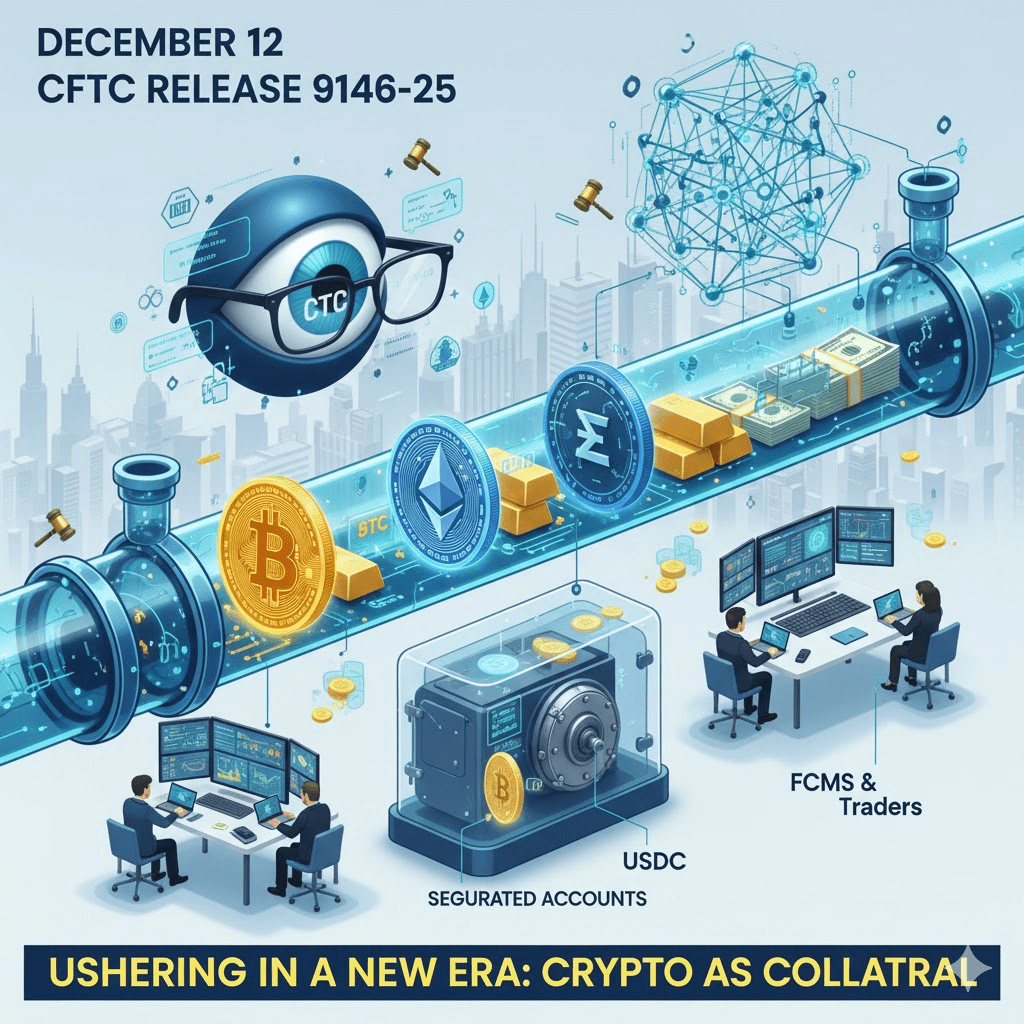

On December 12, the U.S. Commodity Futures Trading Commission (CFTC) announced Release 9146-25 – a document with a long title but a very clear message: Bitcoin, Ethereum, and USDC are officially included in a monitored pilot program, allowing their use as collateral in the U.S. derivatives system.

This is a pilot with many controls, reporting, and detailed regulations, but at the same time marks a substantive change in how the CFTC wants the U.S. market to trade crypto: onshore, under supervision, and minimizing the gap between the assets that investors hold and the market where they hedge risks.

This move coincides with another important milestone: the CFTC has paved the way for crypto spot products to be listed for the first time on the agency's registered exchanges.

Combining these two developments, the direction becomes clear. Instead of pushing crypto to the fringes of the financial system, the CFTC is experimenting with ways to directly integrate them into the same 'pipeline' that operates the futures and swaps market.

The collateral mechanism and why traders need to pay attention

To understand why this pilot program is important, one must grasp the concept of collateral at its simplest level. A derivative transaction can be seen as two parties betting against each other under the supervision of an 'arbitrator.' Since prices can fluctuate very quickly, the arbitrator requires both parties to put up a valuable asset as collateral.

That asset is collateral, ensuring that if the market turns, the transaction can still be settled without needing to trace the losing party.

In reality, the 'arbitrator' is the clearinghouse. The betting parties are the traders. And the entity collecting collateral from customers is the futures commission merchant (FCM) – a high-security intermediary standing between the trader and clearinghouse.

Previously, FCMs almost exclusively accepted USD or U.S. Treasury bonds due to their stability. Crypto was not included due to high volatility, complex custody requirements, and many unresolved legal questions.

Release 9146-25 has changed that. This document outlines how tokenized assets can be used as collateral, the necessary control measures, and the qualifying digital assets for participation. The intentionally limited list includes Bitcoin, Ether, and a regulated stablecoin – USDC. Crypto is given a 'backstage pass' with oversight.

The core content of Release 9146-25

The document consists of two main parts: the digital asset pilot program and the no-action letter for FCMs.

The pilot program is the biggest highlight. It provides a rule framework for exchanges and clearinghouses regarding the use of tokenized assets – including BTC, ETH, USDC, and tokenized U.S. Treasury bonds – for collateral and settlement.

Participants must demonstrate the ability to control wallets, protect customer assets, accurately price, and maintain complete records. This approach leans more towards 'safe operation' than free innovation.

The no-action letter serves as enforcement. It allows FCMs to accept the above assets as customer collateral for a limited time, with strict conditions. At the same time, this document replaces old guidelines that required brokers to avoid 'virtual currencies' in the customer asset segregation mechanism – an approach suitable in 2020 but now outdated as tokenization enters mainstream finance.

Some key points in the pilot phase:

– The first three months are limited in scope: FCMs are only allowed to accept BTC, ETH, and USDC as collateral, in order to collect clean data before expanding.

– Continuous and detailed reporting: FCMs must accurately report weekly the amount of crypto held for customers and the storage position.

– Mandatory asset segregation: Crypto used as collateral must be held in a segregated account, separated from the company's assets and creditors, with a legally effective wallet and audit capability.

– Conservative haircut: Due to higher volatility than bonds, the value of crypto counted as collateral will be discounted.

– Time-limited experiment: The CFTC has not announced an end date, but pilot programs usually last one to two years to observe enough market cycles.

During this time, the CFTC will collect data that old guidelines could not provide: how crypto behaves as collateral in normal markets and during high volatility, how stablecoins operate when backed by leveraged positions, and whether businesses can actually manage on-chain wallets at an organizational level.

Who will be the first participants?

Some businesses are ready to take the lead. Crypto.com, the clearinghouse operator registered with the CFTC, stated that they have supported crypto collateral and tokenization in other markets and can quickly deploy in the U.S.

Other candidates include LedgerX, crypto-native trading firms operating with CME's Bitcoin futures, and those FCMs that have built wallet infrastructure for institutional customers.

In contrast, traditional brokerage firms may be more cautious, as they are not yet accustomed to managing on-chain assets. However, the rewards are very clear: attracting a customer segment that wants to trade on a tightly regulated platform, while still being able to directly use crypto as collateral.

For stablecoin issuers, the inclusion of USDC on the list is a strong signal of the legal framework's suitability. Companies tokenizing U.S. Treasury bonds will also see this as an invitation, even though they must meet stricter custody and legal requirements.

What changes for traders?

The practical impact is most evident in how positions are funded.

A hedge fund trading Bitcoin basis today may have to hold BTC in one place and USD at an FCM in another, constantly rotating capital to meet futures margin. In the pilot model, they could hold that value in BTC and directly submit it as collateral, reducing friction and conversion costs.

For miners, instead of selling BTC for USD just to meet a margin call, they can use their existing BTC holdings as collateral for listed contracts. This keeps more activity in the domestic market and reduces the need for offshore leverage.

Retail investors will not immediately feel the change. Most retail platforms depend on FCMs and will be cautious when accepting highly volatile assets from small accounts. However, as large brokers get involved and the CFTC expands the pilot scope, options like 'using BTC balances as collateral' may gradually emerge.

The bigger picture

For many years, offshore platforms attracted Americans with a simple promise: bring crypto in, use it as collateral, and trade continuously. Domestic exchanges could not compete under the old regulatory framework, causing liquidity to flow outside the oversight of regulators.

The CFTC does not seek to replicate the offshore market. Instead, the agency chooses a cautious approach, testing whether crypto can be integrated into the U.S. system without undermining customer protection, the stability of clearinghouses, or market integrity.

If the experiment is successful, the CFTC will have a template for long-term integration. If it fails, the agency has enough oversight tools to quickly halt the process.

Release 9146-25 acknowledges a reality: the market has been and is using these assets for leverage and hedging. Ignoring that only pushes risk into darker corners. The pilot program brings this activity to light, allowing the CFTC to measure, monitor, and pave a controlled path to modernize the collateral mechanism.

If next year provides clean data and no crises, U.S. traders may finally achieve what they have been hoping for since Bitcoin futures contracts were introduced: domestic trading without having to part with their assets.