Azu is here, brothers. If you are still treating stablecoins as the 'crypto dollars convenient for hedging in exchanges,' then you are really out of sync. The reality is brutal: stablecoins are now part of a multi-trillion dollar 'shadow dollar system,' and the on-chain settlement volume in just one year has already surpassed the total of Visa and Mastercard combined, and it is still accelerating. More importantly, such a huge amount of real demand is still primarily running on a bunch of general-purpose public chains that have not been optimized for 'payments'—transaction fees, gas, congestion, all piled on the ordinary users. Don't you think this is a huge mismatch?

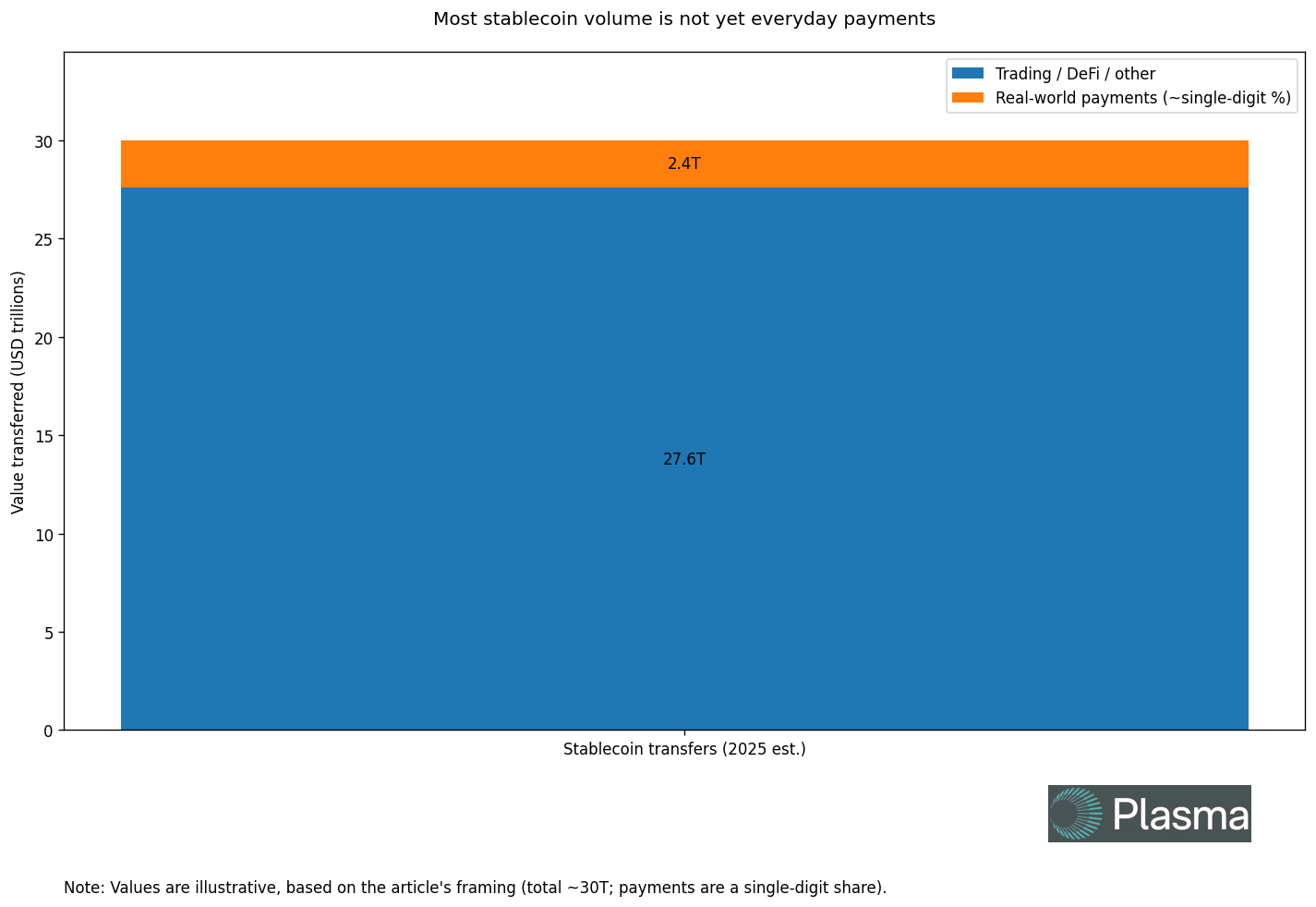

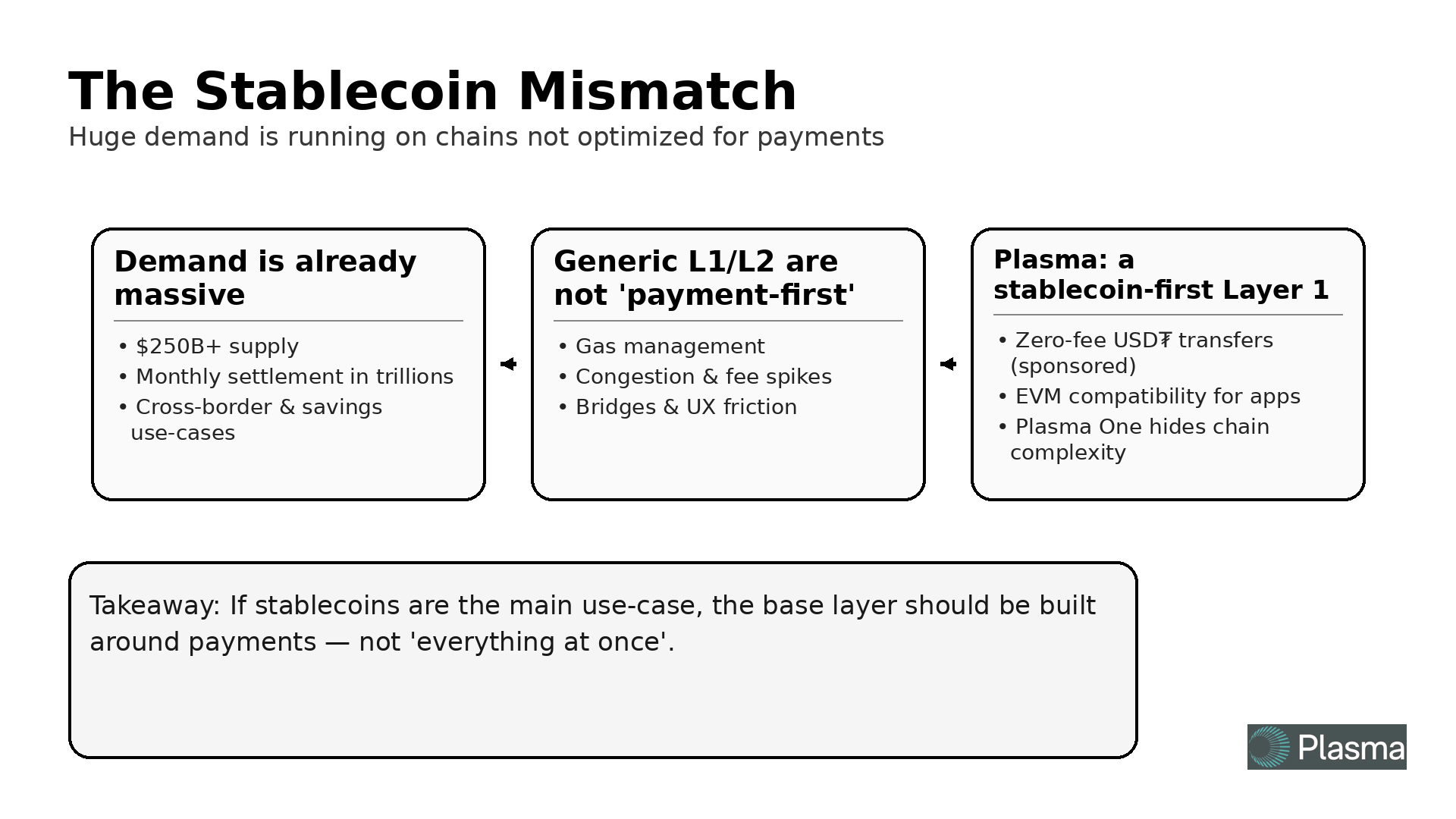

Let's present the data first. The official FAQ of Plasma directly provides a very provocative framing: the current circulation of stablecoins has exceeded $250 billion, with on-chain settlements counted in 'trillions' each month; stablecoins have become the most mainstream use case in the entire crypto world. External research institutions are also emphasizing the same thing in more straightforward language: in 2024, the annual transfer volume of mainstream stablecoins will be in the range of $27–32 trillion, already solidly surpassing traditional card organizations; by 2025, the scale of transactions related to stablecoins will continue to rise, with some statistics directly describing it as 'the value processed is greater than the total of Visa and Mastercard.'

But ironically, among this massive transaction volume, the proportion that is actually linked to real-world payments is still quite small. Analysis data for 2025 shows that stablecoins processed over $30 trillion in on-chain transfers in one year, but only a single-digit percentage was classified as real-world payments; the rest was mostly exchange transfers, DeFi strategies, and bot volume manipulation. What does this mean? It means 'the demand has filled the stadium', but 'the highway specially built for them' has not yet opened, and the main force can only squeeze onto a bunch of temporary roads.

Looking at the problem from the user's perspective is much more intuitive. Think back to your experience using USDT/USDC for these tasks:

Wanting to send some living expenses to family across borders, you first have to buy Gas on a CEX, then bridge the coins back and forth;

Wanting to transfer a small amount of money to a friend, but the gas fees are more glaring than the amount you're sending;

Catching on to on-chain hotspots or bullish market sentiment, even the simplest stablecoin transfer can get stuck in pending for ages.

This is a typical case of 'stablecoins as the main character, public chains as the backstage', but the backstage hasn't seriously decorated the stage for this main character—they were originally created for DeFi, contracts, and NFTs, with payments being just an incidental compatibility.

The entry point of Plasma happens to fall right at this gap. They don't beat around the bush in the official FAQ:

"Plasma is a Layer1 specifically designed for global stablecoin payments. Stablecoins have already become the most mainstream use case in crypto, but have always lacked a truly customized network for them."

In other words, it doesn't first create a chain and then think 'should I build a payment ecosystem', but instead clearly defines from the start: when stablecoins have already reached hundreds of billions in supply and trillions in monthly settlement volume, what kind of network layer should this payment system have? The answer is repeatedly emphasized in Plasma's product line with four words: saving / spending / sending / earning.

This is not just a slogan, but a complete product perspective. If you look at the introduction of Plasma One, you'll find that it wasn't thinking about 'telling the story from the chain' at all, but rather starting directly from the user account:

Using stablecoins to save money while casually earning on-chain returns;

When consuming with a card, the money is directly deducted from this pile of stablecoins, without forcing you to convert to other assets during the process;

Transfers are zero-fee USD₮ transfers, just like sending a message;

The entire process, combined with cashback, points, and global merchant acceptance, makes you forget 'I'm using the chain.'

In other words, Plasma One is more like using a layer of 'new digital banks + card organizations' skin to conceal the stablecoin payment chain behind. What you hold are cards and apps, but what you are using in the background is a settlement layer customized for stablecoin payments. This is why I particularly use 'demand-side' to tell the story while writing this: it's not that the chain exists first and the demand comes later; rather, the demand has surged to the point that we have to build a dedicated path for it.

So why is it 'now' at this moment? From macro to industry, you'll find a bunch of interesting resonance points. On the side of traditional institutions, Visa itself is publicly stating: every bank should have a stablecoin strategy in the coming years, treating stablecoins as the foundational components for the next generation of cross-border transactions, clearing, and enterprise payments. On the other hand, various reports have already included the annual settlement volume of stablecoins in mainstream payment discussions: approximately $27.6 trillion in stablecoin on-chain transfers in 2024, over $30 trillion in total transactions in 2025, which is on a completely different level from the growth rate of card organizations.

However, the vast majority of these settlement flows are currently in a state of 'making do':

Using a general public chain optimized for DeFi;

Sharing a congested environment with high-frequency trading and MEV block grabbing;

Every on-chain payment has to bear the side effect of 'this is not tailor-made for you.'

It's like using a high-frequency quantitative trading channel to run payroll and cross-border B2B settlements; of course it can run, but the experience is definitely weird—delays, rates, stability, all mismatched with the scenario. The demand curve for stablecoins has already grown into a big tree, but the underlying soil is still a few bricks temporarily propped up.

What Plasma aims to do is replace this layer of 'soil'. If you look at both the FAQ and the white paper, you'll find that it has a very distinct design philosophy:

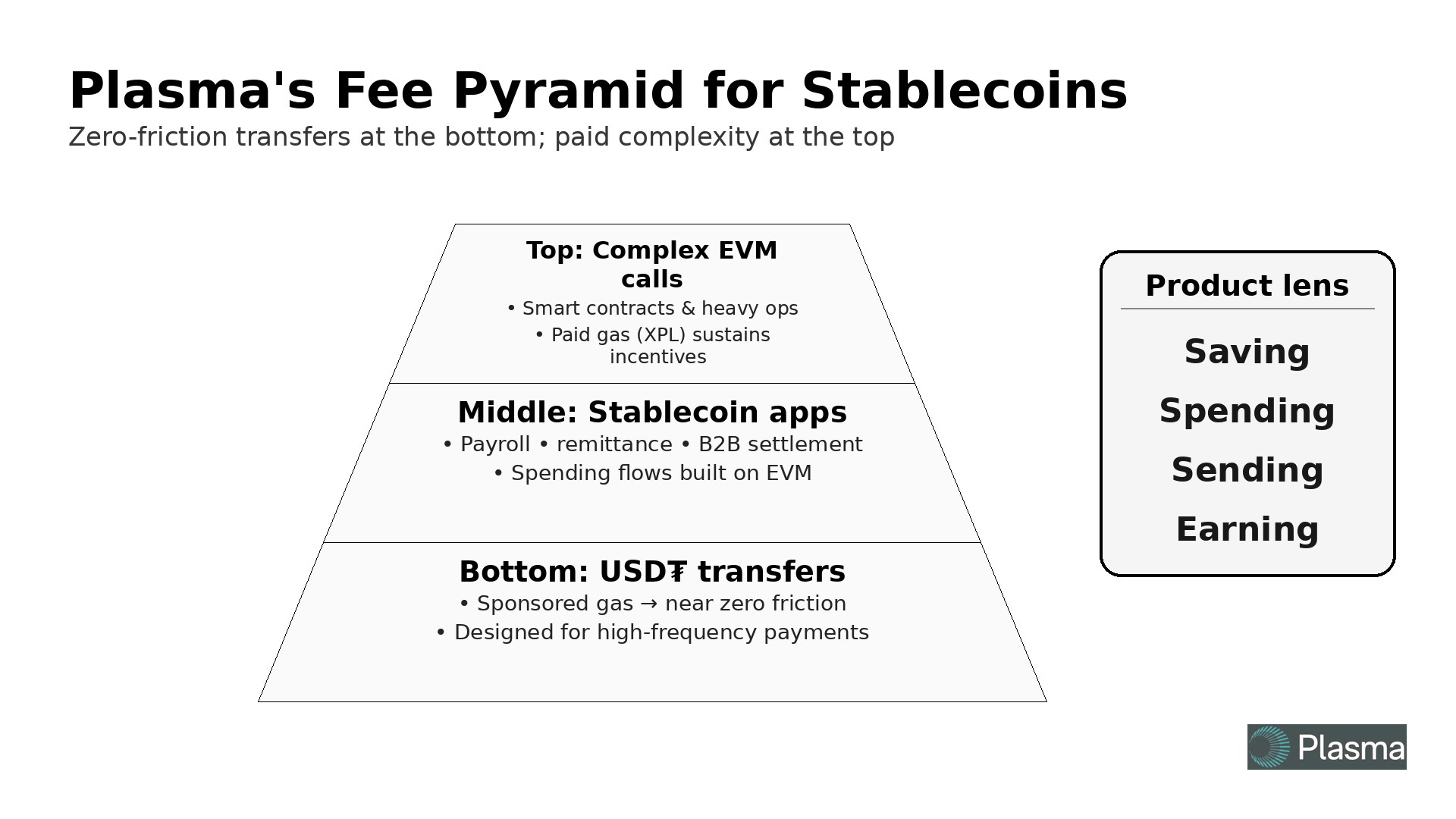

At the bottom layer is PlasmaBFT + Reth EVM, this combination is not meant for playing complex financial magic but for the throughput and certainty of 'stablecoin scale';

The network level directly integrates zero-fee USD₮ transfers, using a protocol layer paymaster to sponsor purely USDT transfers, making the most frequent and basic payment paths nearly frictionless;

More complex transactions and contract calls still require using XPL to pay fees, ensuring the entire system's economic closure and validator incentives.

The key detail here is 'who pays for the payment experience'. On traditional public chains, either the user pays for it themselves—first going to get a bunch of gas; or some app privately subsidizes you—sending some points, pulling some operation budget, until there's no money left. Plasma moves this mechanism forward to the protocol:

The most basic USD₮ transfers are sponsored by the network layer for gas, improving the experience of the four core actions of 'saving / spending / sending / earning';

Only when you perform heavier contract calls or high-complexity operations do you need to revert to the 'normal XPL payment' path.

From the results, this has turned stablecoin payments into a very clear pyramid: at the bottom are massive high-frequency, small, scenario-based transfers, free, smooth, and low mental burden; above are various payment/investment/settlement applications built around stablecoins, willing to pay for more complex functions; at the top are infrastructure participants, validators, and bridge players, distributing benefits and risks using this economic system of XPL.

For developers and businesses, that 'saving / spending / sending / earning' set is actually a very straightforward product demand statement. Plasma directly states in the FAQ: the applications we most want to see are those that focus on these four actions—cross-border remittances, payroll, B2B settlements, consumer finance, card organization interactions, API acquisitions... as long as the main subject of your business is 'how stablecoins flow in reality', then this chain is your 'dedicated lane.'

So, when I say 'why is now the right time to talk about Plasma's Day 2', I'm actually talking about something much more fundamental: stablecoins have already transitioned from 'narrative' to 'infrastructure', but many transactions are still running on the wrong tracks. Stablecoin use cases have long moved from exchanges to cross-border remittances, freelance income, asset hedging, and global consumption, but the underlying infrastructure we have for them is still optimized for DeFi and speculation from a few years ago. The value of Plasma lies in its acknowledgment of a simple fact—when a use case has already become the largest demand pool, you shouldn't serve it with 'a chain that does a little bit of everything', but rather build a settlement layer centered around it.

From the standpoint of Azu, my view on Plasma can be summarized in a single sentence: it is one of the few that is willing to design the underlying layer starting from the reality that 'stablecoins have already beaten Visa'. It doesn't say it wants to launch a new chain to compete for TVL but honestly acknowledges: in the coming years, what will determine the life and death of this chain is whether these four actions of 'saving / spending / sending / earning' can become smoother, more stable, and cheaper here than elsewhere.

I want to clarify this 'demand-side story' first, and then we can break it down bit by bit in the coming days: the engineering details behind zero-fee USD₮, what PlasmaBFT + Reth have done for the scale of stablecoins, what role XPL plays in this machine, and how ordinary users will actually engage with this system.

In your own on-chain life, are stablecoins now more about 'trading', 'saving', or have they already become 'money to spend'? What do you think is the most unreasonable pain point: transaction fees, Gas, or that feeling of helplessness when congestion hits and you can't do anything?

Feel free to express your experiences in the comments; I will continue to keep an eye on it.@Plasma This chain will help you uncover all the verifiable data.