Written by: Artemis Analytics

Compiled by: Web3 Lawyer

We are often misled by the exaggerated stablecoin trading volumes in article titles, immersed in the excitement of it surpassing V/M trading volume, dreaming of 'planning cancellation, preparing to take the championship' to replace SWIFT. Comparing the trading volume of stablecoins to Visa/Mastercard is like comparing the volume of securities settlement funds to Visa/Mastercard; they are not comparable.

Although blockchain data shows that stablecoin trading volume is huge, most of it does not represent real-world payments.

Currently, the majority of stablecoin trading volume comes from: 1) Capital balances of exchanges and custodians; 2) Trading, arbitrage, and liquidity cycles; 3) Smart contract mechanisms; 4) Financial adjustments.

Blockchain only shows the transfer of value, not why they transfer. Therefore, we need to clarify the actual funding routes used for payments behind stablecoins and the statistical logic. Accordingly, we compiled the article Stablecoins in payments: What the raw transaction numbers miss, McKinsey & Artemis Analytics, aimed at helping us clear the fog around stablecoin payments and see the reality.

https://www.linkedin.com/pulse/stablecoins-payments-what-raw-transaction-numbers-4qjke/?trackingId=tjIPCCnHTE6N72YmfMWHVA%3D%3D

According to the analysis results of Artemis Analytics, the actual scale of stablecoin payments in 2025 is approximately $390 billion, doubling from 2024.

It should be noted that actual stablecoin payments are far below conventional estimates, but this does not diminish the long-term potential of stablecoins as a payment channel. On the contrary, this provides a clearer benchmark for assessing the current state of the market and the conditions required for the large-scale development of stablecoins. At the same time, we can also clearly see that stablecoins truly exist in the payment field, are growing, and are in the early stages. The opportunities are immense; it just requires the correct measurement of these numbers.

I. Overall Transaction Volume of Stablecoins

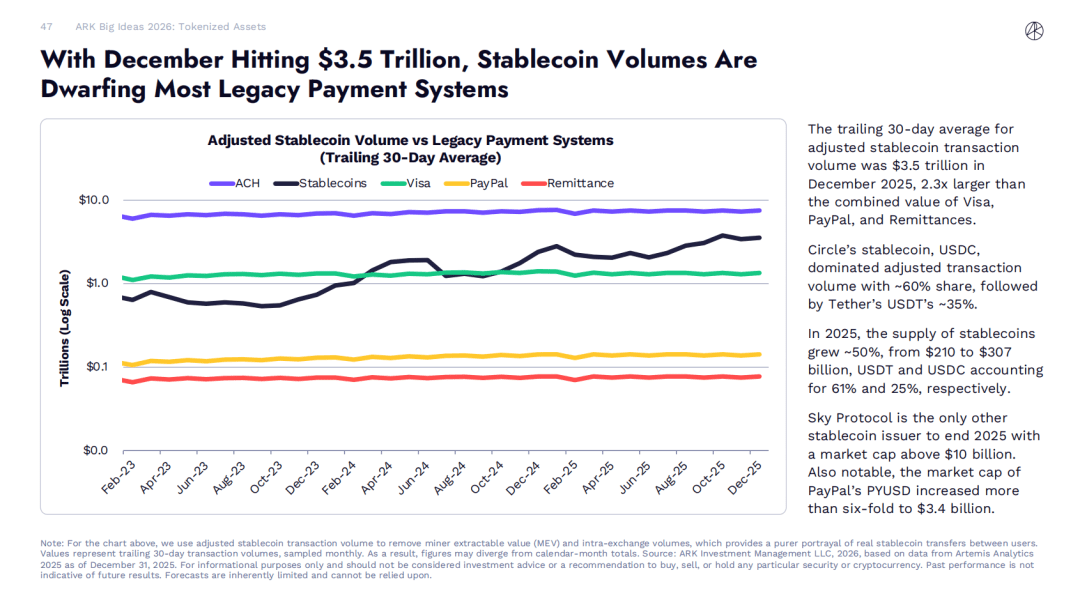

Stablecoins are increasingly being recognized as a faster, cheaper, and programmable payment solution. According to reports from Artemis Analytics, Allium, RWA.xyz, and Dune Analytics, their annual transaction volume reaches up to $35 trillion.

ARK Invest 2026 Big Ideas data shows that by December 2025, the adjusted 30-day moving average of stablecoin transaction volume is $35 trillion, which is 2.3 times that of the total of Visa, PayPal, and remittance businesses.

However, most of these transaction activities are not genuine end-user payments, such as payments to suppliers or remittances. They mainly include trading, internal fund transfers, and automated blockchain activities.

To eliminate interference factors and more accurately assess stablecoin payment volumes, McKinsey collaborated with leading blockchain analysis provider Artemis Analytics. The analysis results indicate:

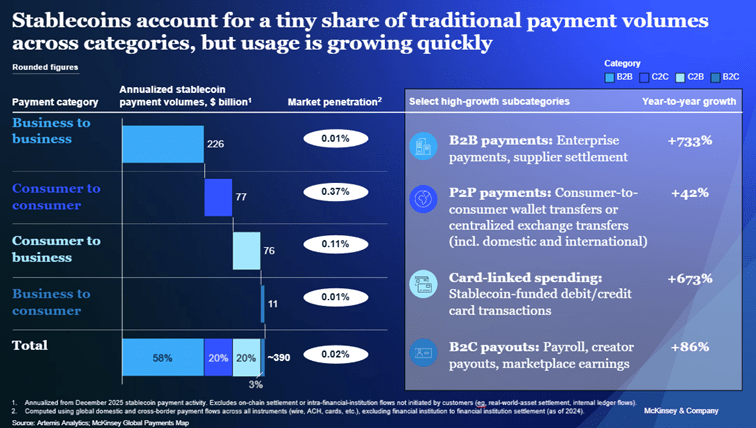

Based on the current transaction speed (annualized figures based on stablecoin payment activity in December 2025), the actual annual stablecoin payment volume is approximately $390 billion, accounting for about 0.02% of the total global payment volume.

This highlights the necessity for more detailed interpretations of the data recorded on the blockchain, and the need for financial institutions to make strategically oriented investments based on application scenarios to realize the long-term potential of stablecoins.

II. Strong Growth Expectations for Stablecoins

In recent years, the stablecoin market has expanded rapidly, with its circulating supply surpassing $300 billion, compared to less than $30 billion in 2020 (DeFillma data).

Market public forecasts indicate a strong expectation for continued growth in the stablecoin market. On November 12 last year, U.S. Treasury Secretary Scott Bensinger stated in a speech at the Treasury market conference that by 2030, the supply of stablecoins could reach $3 trillion.

Leading financial institutions have made similar predictions, estimating that the supply of stablecoins will fall within the range of $2 trillion to $4 trillion during the same period. This growth expectation has significantly increased the attention of financial institutions towards stablecoins, with many institutions exploring the application of stablecoins in various payment and settlement scenarios.

When you filter out payment-like behaviors, a completely different picture emerges, with uneven adoption across various scenarios:

Global salaries and cross-border remittances: Stablecoins provide a highly attractive alternative to traditional remittance channels, enabling near-instantaneous cross-border fund transfers at very low costs. According to McKinsey's Global Payments Map data, the annualized payment scale of stablecoins in the global salary and cross-border remittance sectors is approximately $90 billion, with the overall transaction scale in this field reaching $1.2 trillion, of which stablecoins account for less than 1%.

B2B payments between enterprises: Cross-border payments and international trade have long faced efficiency pain points such as high fees and long settlement cycles, and stablecoins happen to solve these problems. Enterprises that take the lead in adopting stablecoins are optimizing supply chain payment processes and improving liquidity management, with small and micro enterprises benefiting particularly significantly. According to McKinsey's Global Payments Map data, the annualized scale of stablecoin inter-enterprise payments is approximately $226 trillion, while the overall scale of global inter-enterprise payments is about $1.6 trillion, with stablecoins accounting for only about 0.01%.

Capital markets: Stablecoins are reshaping the settlement processes in capital markets by reducing counterparty risk and shortening settlement cycles. Some tokenized funds issued by asset management firms have already achieved automatic dividend distribution to investors via stablecoins or directly reinvesting dividends into the fund without going through banks for fund transfers. This early application scenario fully demonstrates that on-chain cash flow can effectively simplify the operational processes of funds. Data shows that the annualized settlement transaction scale of stablecoins in capital markets is approximately $8 billion, while the overall settlement scale of global capital markets reaches $200 trillion, with stablecoins accounting for less than 0.01%.

Currently, the evidence cited by various parties to support the rapid adoption of stablecoins is mostly based on publicly available stablecoin transaction scale data, and people often assume that this data can reflect actual payment activities. However, to judge whether these transactions are related to payment behaviors, a deeper analysis of the actual connotation of on-chain transactions is required.

(https://x.com/artemis/status/2014742549236482078)

Currently, the majority of real stablecoin payment transaction volumes are highly concentrated in Asia, with regions like Singapore, Hong Kong, and Japan being at least one of the transaction channels. Global saturation has not yet been achieved.

Although the above market predictions and early application scenarios affirm the significant growth potential of stablecoins, they also reveal a reality: there remains a considerable gap between market expectations and the actual situation that can be derived solely from surface transaction data.

McKinsey & Company, Global Payments Map

https://www.mckinsey.com/industries/financial-services/how-we-help-clients/gci-analytics/our-offerings/global-payments-map

III. Prudent Interpretation of Stablecoin Transaction Volume

Public blockchains provide unprecedented transparency for transaction activities: every fund transfer is recorded on a shared ledger, allowing people to almost real-time grasp the flow of funds between wallets and various applications.

Theoretically, compared to traditional payment systems, this characteristic of blockchain makes it more convenient for the market to assess the level of stablecoin adoption — the transaction data of traditional payment systems is dispersed across various private networks, only disclosing aggregated data, and some transactions are not disclosed at all.

However, in practical operations, the total transaction scale of stablecoins cannot be directly equated to the actual payment scale.

Public blockchain transaction data can only reflect the amount of fund transfers and cannot reflect the economic purposes behind them. Therefore, the raw stablecoin transaction scale on the blockchain actually includes various types of transactional behaviors, specifically including:

Cryptocurrency exchanges and custodians hold large reserves of stablecoins and transfer funds between their own wallets;

Smart contracts interact automatically, leading to the same funds being transferred repeatedly;

Liquidity management, arbitrage, and fund flows related to trading;

Technical mechanisms at the protocol level break down single operations into multiple on-chain operations, resulting in multiple blockchain transactions that inflate the total transaction scale.

These behaviors are important components of the on-chain ecosystem and are likely to further grow with the widespread adoption of stablecoins. However, from a traditional definition, most of these behaviors do not fall under the category of payments. If they are aggregated without adjustment, it will obscure the true scale of actual stablecoin payment activities.

This provides a very clear insight for financial institutions assessing stablecoins:

Publicly available raw transaction scale data can only serve as a starting point for analysis; it cannot be equated to the adoption level of stablecoin payments, nor can it be seen as the actual revenue scale that stablecoin businesses can generate.

IV. The Landscape of Actual Stablecoin Payment Scale

In an analysis conducted in collaboration with Artemis Analytics, a detailed breakdown of stablecoin transaction data was performed. The study focused on identifying transaction patterns that meet payment characteristics, including commercial fund transfers, settlements, payroll distributions, cross-border remittances, etc., while excluding transaction data primarily focused on trading, internal fund rebalancing, and automated smart contract cycles.

The analysis results show that the actual scale of stablecoin payments in 2025 is approximately $390 billion, doubling from 2024. Although the scale of stablecoin transactions in the overall on-chain transactions and the global total payment scale remains relatively low, this data is sufficient to confirm that stablecoins have formed real and continuously growing application demand in specific scenarios (see charts).

(Stablecoins in payments: What the raw transaction numbers miss)

Our analysis has yielded three prominent observations:

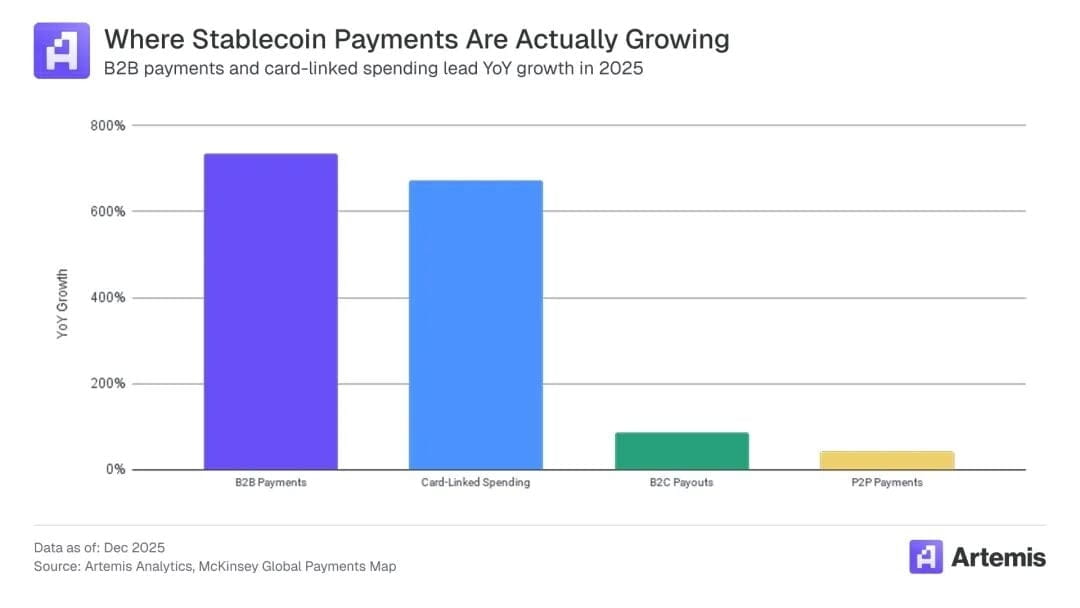

Clear value proposition. The reason stablecoins are becoming increasingly popular is that they offer significant advantages over existing payment channels, such as faster settlement speeds, better liquidity management, and lower user experience friction. For example, we estimate that by 2026, the consumption amount of stablecoin-linked bank cards will grow to $4.5 billion, an increase of 673% compared to 2024.

B2B leads growth. B2B payments dominate, amounting to approximately $226 billion, accounting for about 60% of the total global stablecoin payments. B2B payments have increased by 733% year-on-year, indicating that 2026 will see rapid growth.

Transaction activities are most active in the Asian region. The transaction activities across different regions and cross-border payment channels are uneven, indicating that the transaction scale will depend on the local market structure and limiting factors. Stablecoin payments from Asia are the largest source of transactions, with a transaction volume of approximately $245 billion, accounting for 60% of the total. North America follows with a transaction volume of $95 billion, while Europe ranks third with $50 billion. Latin America and Africa have transaction volumes of less than $1 billion each. Currently, transaction activities are almost entirely driven by payments from Singapore, Hong Kong, and Japan.

In summary, the above trends indicate that the application of stablecoins is gradually taking root in a few verified scenarios, and whether they can achieve broader large-scale development hinges on whether these mature scenario models can be successfully promoted and replicated in other regions.

Stablecoins have substantial potential to reshape the payment system, and the release of this potential relies on ongoing technological research and development, regulatory improvements, and the continuous advancement of market implementation. Their large-scale application requires clearer data analysis, more rational investment layouts, and the ability to discern effective signals from public transaction data while filtering out invalid noise. For financial institutions, only by harboring development ambitions while objectively recognizing the current state of stablecoin transaction scales and steadily laying out future development opportunities can they seize the initiative in the next stage of stablecoin applications and lead industry development.