Imagine this: $BTC hits a new high, a fresh Solana or $XRP ETF launches, crypto Twitter is euphoric… and yet SOL and XRP start dumping right after the “bullish” ETF news.

Now, let's take a look what a crypto ETF actually is, how it works, why it’s different from simply buying coins yourself, and why altcoin prices can still fall even after “successful” spot ETF launches.

What Is a Crypto ETF?

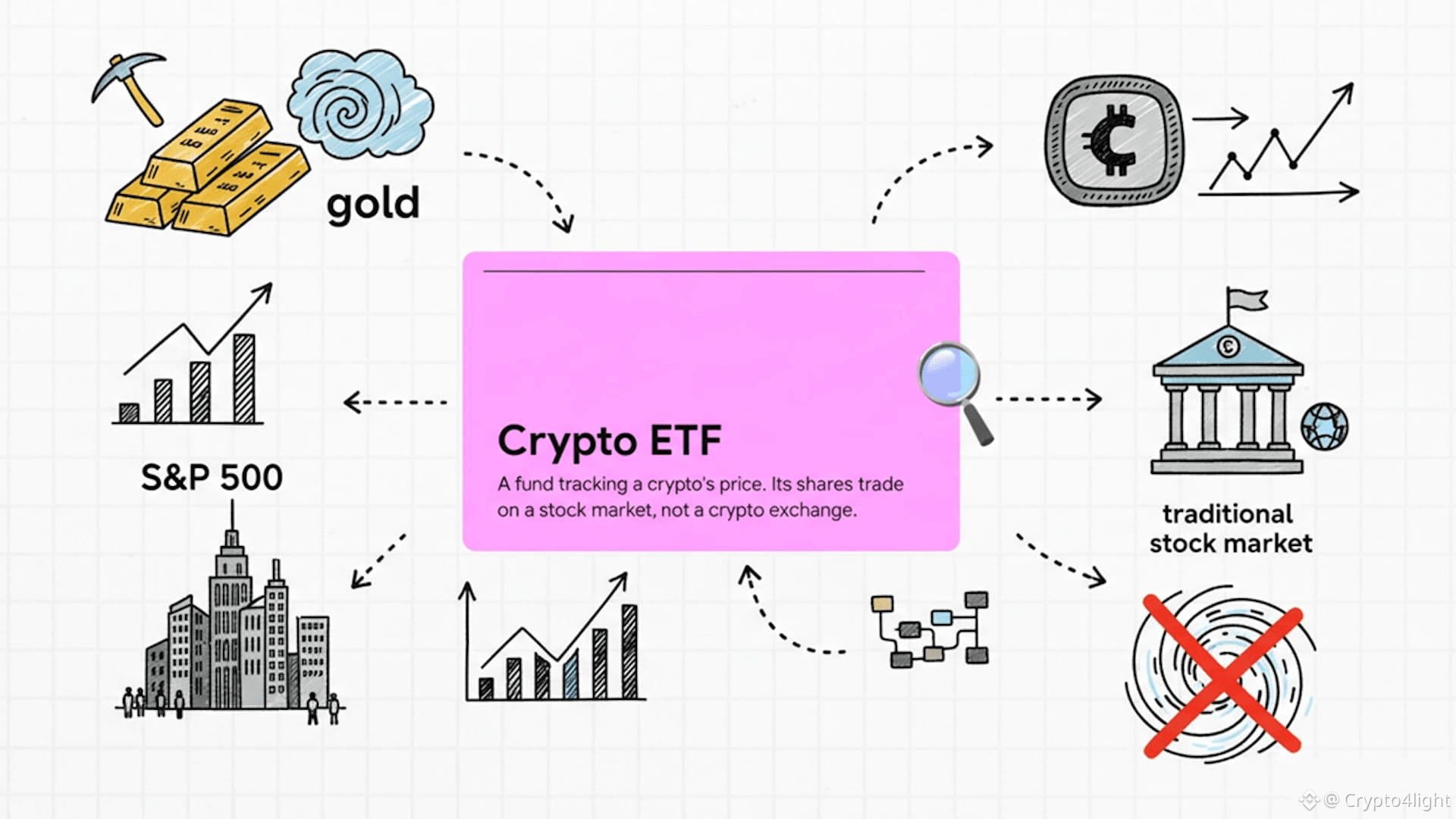

Let’s start with the basics – a crypto ETF, or exchange‑traded fund, is a traditional investment fund whose job is to track the price of one cryptocurrency or a basket of cryptocurrencies.

Instead of buying Bitcoin, Ethereum or altcoins directly on an exchange, an investor buys shares of this fund on a stock market, just like buying shares of an S&P 500 ETF or a gold ETF.

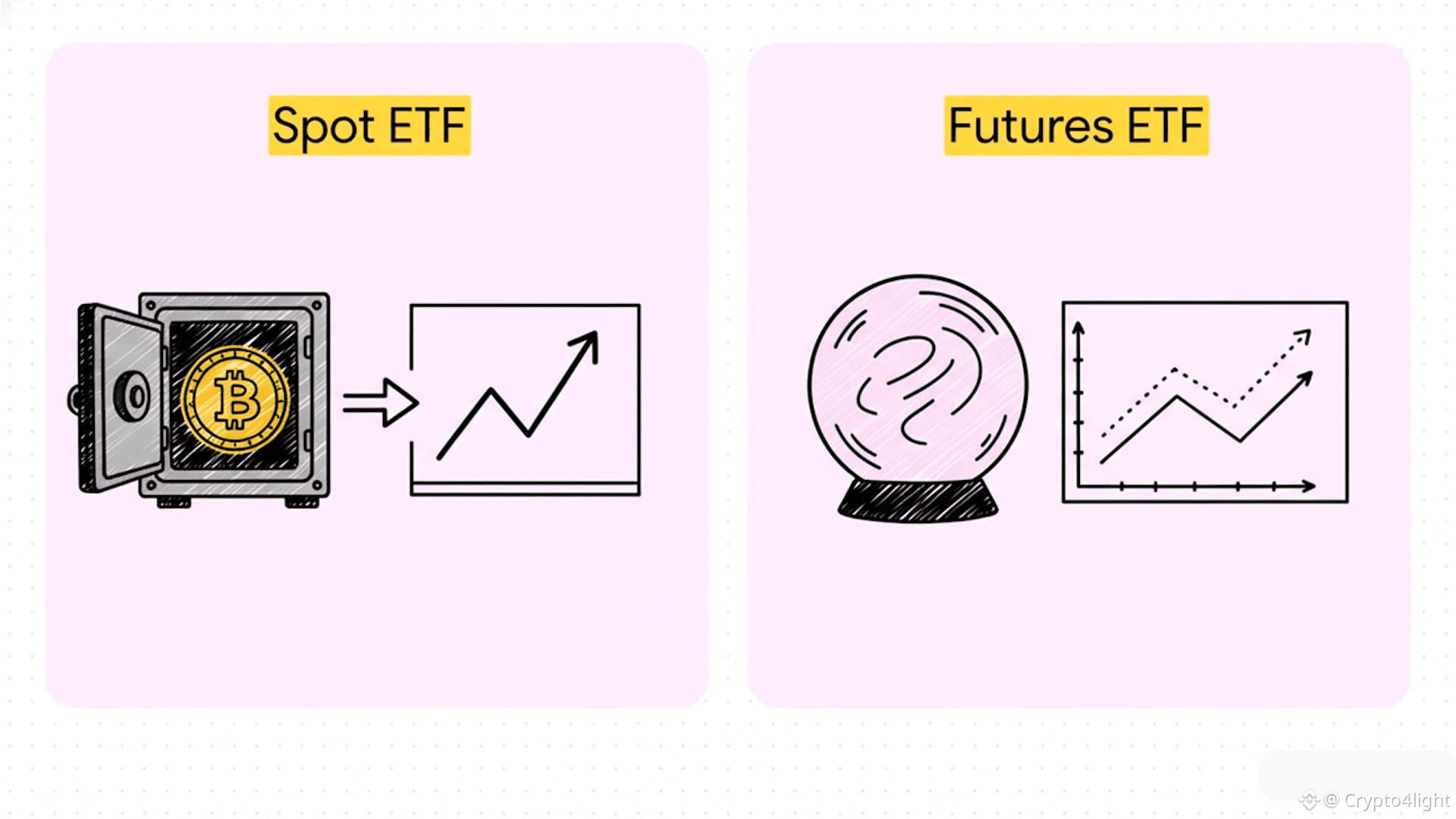

There are two main types of crypto ETFs investors usually talk about.

Spot crypto ETFs hold the underlying asset directly – for example, a spot Bitcoin ETF actually owns BTC in custody, and its share price reflects real‑time Bitcoin movements, minus fees.

Futures crypto ETFs do not hold coins; instead, they hold futures contracts, which can lead to tracking errors when futures prices diverge from spot prices over time.

How Does a Spot Crypto ETF Work?

Now, how does a spot crypto ETF actually operate behind the scenes?

At the center is the fund issuer – a company that sets up the ETF and decides its rules, fees, and which custodian will hold the coins.

The issuer’s goal is simple: make the ETF share price follow the underlying crypto price as closely as possible, whether that’s BTC, ETH, SOL, XRP or a basket of assets.

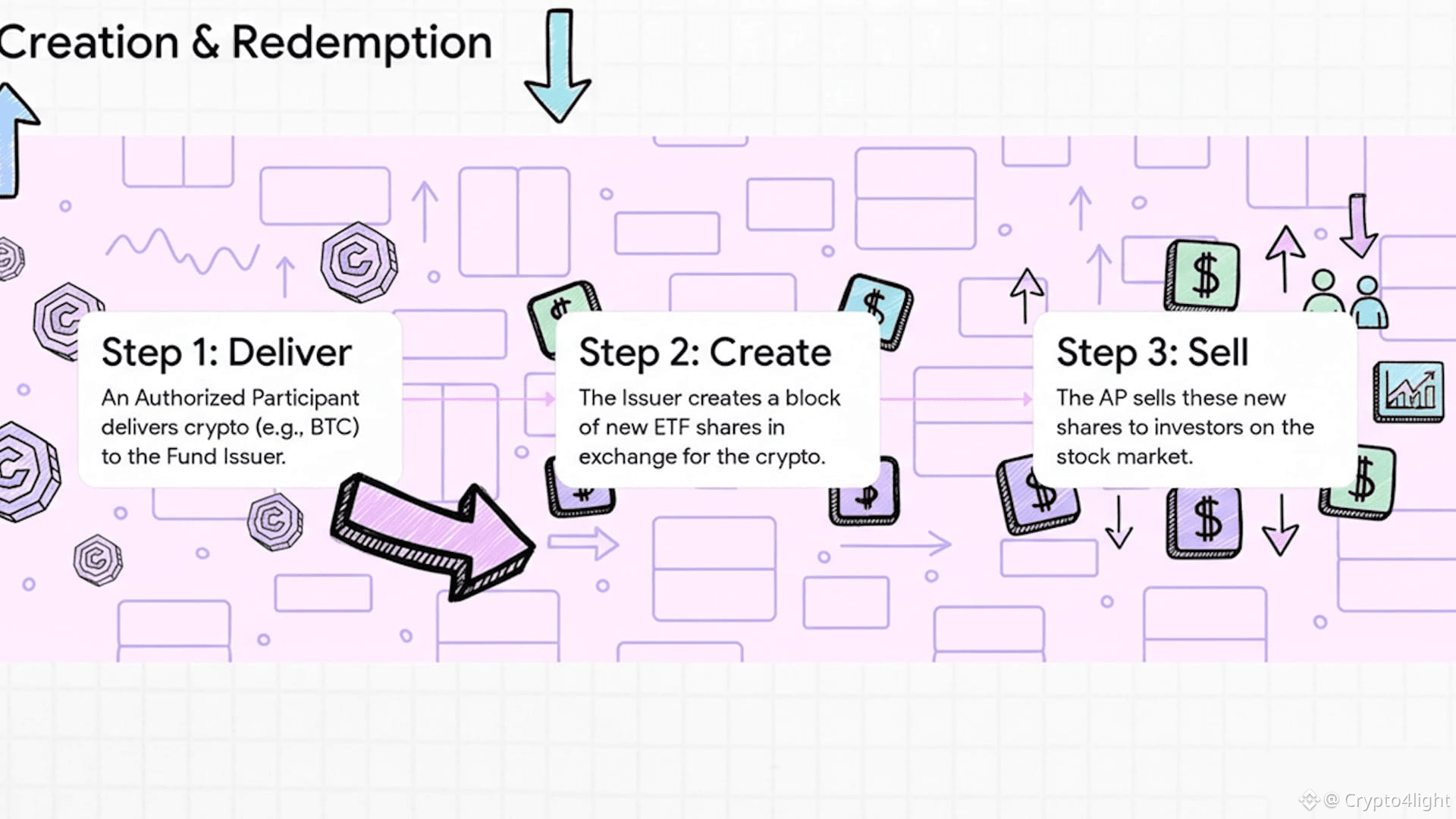

The key mechanism is called “creation and redemption.”

Authorized participants (large institutions or market makers) deliver Bitcoin or another crypto to the fund in exchange for big blocks of new ETF shares, called creation units.

They can also return ETF shares to the fund and receive the underlying coins or cash back, which is called redemption, keeping ETF price aligned with the spot market.

Retail investors never see this process.

A regular investor just opens a brokerage app, types in the ETF ticker (for example a Bitcoin or Solana ETF), and buys or sells shares during normal stock market hours using fiat.

Even though the ETF is backed by crypto, shareholders typically cannot redeem those shares for actual coins; they only get exposure to price changes, not direct control over wallets or private keys.

ETF vs Buying Crypto Directly

So what is the difference between buying a crypto ETF and buying the coin itself on an exchange?

First, ownership and control are completely different.

When you buy the coin directly (BTC, ETH, SOL, XRP), you can move it to your own wallet, stake it, use it in DeFi, or send it anywhere – you control the private keys and the asset itself.

When you buy a crypto ETF, you only own shares of a regulated fund; you cannot withdraw ETF shares as real coins, interact with blockchains, or use DeFi protocols with those shares.

Second, the access and regulation side looks very different.

ETFs trade on traditional stock exchanges and are regulated as securities, which means many conservative investors, pension funds, and institutions feel more comfortable using them instead of opening accounts on crypto exchanges.

Direct crypto purchase requires dealing with exchanges, wallets, KYC on new platforms, self‑custody risks, and sometimes unclear regulation, which many traditional investors want to avoid.

Third, fees, trading hours and tax treatment are not the same.

ETFs charge an annual management fee and only trade during market hours, while spot crypto trades 24/7 but has exchange fees, spreads, and custody risks instead.

In many jurisdictions, ETFs may have clearer tax reporting, whereas direct crypto can fall into less familiar tax categories for mainstream investors and their accountants.

Suppose there is a spot Solana ETF backed by SOL that trades on a major stock exchange; a traditional investor can buy “SOL exposure” at the click of a button without ever touching a crypto wallet.

Meanwhile, a crypto‑native user might prefer to buy SOL directly on Binance or another exchange, stake it on‑chain, and bridge it between DeFi platforms – something an ETF simply cannot offer.

Why Launch Bitcoin and Altcoin ETFs At All?

Now let’s answer the big “why” – why launch ETFs for Bitcoin, and even more, for altcoins?

From the perspective of traditional finance, ETFs are a bridge product.

Crypto ETFs let banks, asset managers, and pension funds offer “crypto exposure” in a familiar, regulated wrapper without forcing their clients into new platforms or custody models.

This increases potential capital inflows over time, boosts market legitimacy, and integrates crypto into standard investment portfolios alongside stocks and bonds.

For regulators and policymakers, ETFs are easier to supervise.

Instead of millions of retail users self‑custodying coins and getting hacked or scammed, regulators can oversee a smaller number of large funds and custodians with strict compliance obligations.

In practice, this is why spot Bitcoin and later Ethereum ETFs were approved only after years of debate – they align crypto more closely with existing financial rules and investor protection frameworks.

Now, why ETFs for altcoins like Solana or XRP?

Altcoin ETFs expand the investable universe: they allow institutions to express views beyond Bitcoin and Ethereum, for example on high‑throughput chains or payment‑focused networks.

They also create new fee streams for issuers and trading venues, which is why there is strong business incentive to launch products for any asset with sufficient demand and liquidity.

However, it is important to stress that launching an ETF does not magically create new value for the underlying protocol.

An ETF does not change Solana’s transaction throughput, XRP’s adoption by payment providers, or any chain’s tokenomics; it only changes how investors can gain exposure.

Over the long term, fundamentals, on‑chain activity, and macro conditions still dominate price performance, with ETFs acting more like a new distribution channel than a fundamental upgrade.

Why Can Altcoin Prices Fall After Spot ETF Launches?

This is the paradox many viewers are interested in: “If a spot ETF is bullish, why does the coin dump?” Let’s break down the main reasons, using altcoin examples.

First, there is the classic “buy the rumor, sell the news” dynamic.

In the weeks before a big ETF launch, traders front‑run the narrative, pushing prices higher on expectations of fresh inflows and institutional FOMO.

Once the ETF is live, early speculators lock in profits, and selling pressure from those who “bought the rumor” can outweigh the actual new demand from ETF buyers, causing the price to drop.

Second, inflows are often overstated or misunderstood.

Headline numbers such as “record first‑day ETF volume” may include a lot of short‑term trading, arbitrage, and hedging, not pure net buying from new long‑term investors.

Many institutional players buy ETF shares while simultaneously shorting the underlying coin or futures to run market‑neutral strategies, which adds selling pressure on spot markets instead of relieving it.

Third, capital rotation within crypto can mask or fully offset ETF demand.

In some altcoin cases, strong ETF demand has been driven by investors rotating out of Bitcoin or Ethereum into alt exposure, rather than bringing in completely new money from outside crypto.

If the total crypto market cap is under pressure due to macro factors – for example, higher interest rates or risk‑off sentiment – this internal reshuffling does little to support prices and may even accelerate drawdowns.

Fourth, macro environment and timing matter a lot.

When certain Solana and XRP ETFs launched, this happened during a broader risk‑off phase where Bitcoin itself had already started a significant decline from its highs, dragging the entire market lower.

In such conditions, even “successful” ETFs with healthy inflows cannot fully counteract selling pressure from leveraged liquidations, profit‑taking, or capital leaving the asset class entirely.

Fifth, ETF structure and initial allocations can delay the impact on spot markets.

Some funds accept either the altcoin or fiat in big “baskets” – for example 10,000‑coin blocks – from authorized participants when creating new shares.

If APs mostly deliver coins they already hold from exchanges and custodians rather than buying fresh tokens on the open market, ETF creation does not translate into strong spot‑market buy pressure at launch.

To tie this together with a concrete scenario for your viewers:

Imagine SOL rallies from 180 to over 200 dollars in the days before its ETF goes live, driven by traders expecting a “second leg up” once traditional investors can buy via the ETF.

The ETF launches, initial flows are solid on paper, but large holders and leveraged longs start taking profits, market‑neutral strategies add selling, macro is risk‑off, and SOL slides from around 205 toward the 140 area over the next weeks, despite headlines about “record” ETF metrics.

An ETF is an access tool and a narrative catalyst, not a guaranteed price pump, especially in the short term.

Over time, if ETFs steadily attract net new capital from outside the crypto ecosystem, they can support higher valuations, but that effect is gradual and heavily dependent on macro and fundamentals.