If you’re looking at Plasma right now and thinking “why is a stablecoin settlement chain even getting attention when every chain claims it can do payments,” the tape is basically answering that for you. $XPL has been trading around the $0.12 handle with real liquidity behind it, roughly ~$90M-ish in 24h volume and a ~$200M+ market cap depending on the tracker, after putting in an early peak around $1.68 back in late September 2025. That’s not sleepy, forgotten alt behavior. That’s the market actively repricing what “stablecoin-first” might be worth if adoption shows up in the places that matter.

Stablecoins Are the Rails People Actually Use

Now here’s the thing. Stablecoins have quietly become the settlement layer people actually use, not the one they talk about on podcasts. Total stablecoin supply is sitting around the low $300B range in early 2026, and alone is around the high $180B range in USDT outstanding depending on the snapshot you’re looking at. That concentration matters because it tells you where the payment “gravity” lives, and it also tells you the competition is not theoretical. You’re not competing with vibes, you’re competing with the default rails people already route size through.

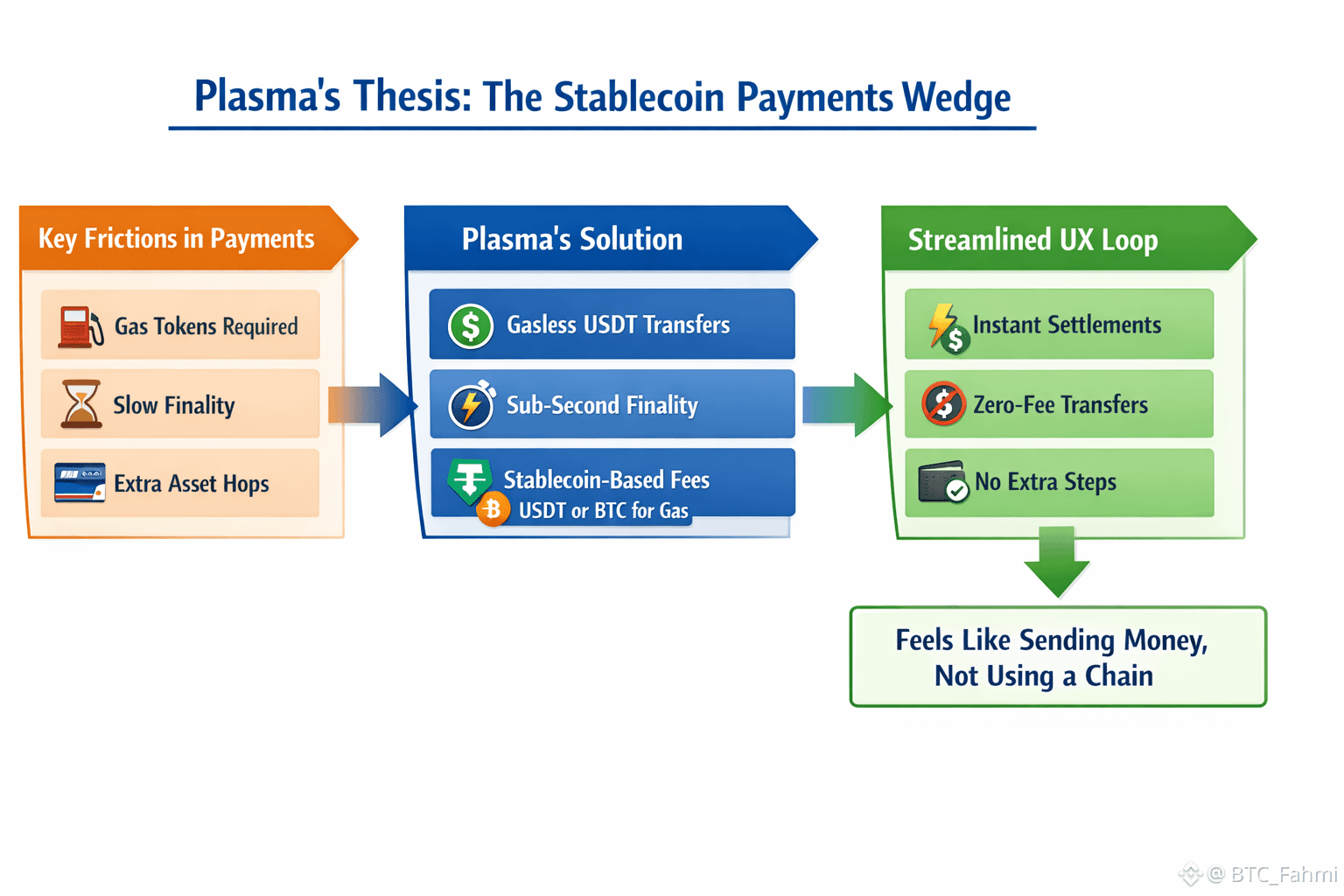

Plasma’s Wedge: Remove Gas Friction + Make Finality Feel Like Money

So what’s Plasma’s actual wedge in a brutally crowded on-chain settlement arena? It’s not “we’re faster” in the abstract. Plasma is explicitly trying to remove the two frictions that kill stablecoin payments at scale: needing a separate gas token, and waiting long enough for finality that the receiver treats the transfer like a promise instead of money. The design choices are pretty on-the-nose: zero-fee USD₮ transfers, stablecoin-first gas where fees can be paid in USD₮ (and even BTC via auto-swap), and sub-second finality via its PlasmaBFT consensus. And then it tries to borrow a credibility shortcut with Bitcoin-anchored security, basically saying “we want the settlement assurances to rhyme with the most conservative base layer.” That’s a specific product thesis, not a generic L1 pitch.

The “Metro Card” Problem: Payments Users Hate Extra Asset Hops

Think of it like this. Most chains make you buy a metro card before you can ride the train, and they tell you it’s fine because the card is “part of the economy.” Payments users hate that. If the product is dollars moving, forcing an extra asset hop is friction and friction turns into churn. Gasless USDT transfers are Plasma trying to make the “metro card” invisible for the common case. Then stablecoin-first gas is the fallback for everything that isn’t the common case, so developers can still build real apps without forcing users into the native-token tax on day one. If Plasma nails that UX loop, it doesn’t need to win a narrative war. It needs to win the default routing decision for wallets, merchants, and remitters who already think in stablecoins.

Competitive Reality: You’re Fighting Incumbent Flow, Not Theory

This is where the competition gets fierce, because everyone can see the same opportunity. has been the workhorse rail for USDT transfers for a long time because it’s cheap, predictable, and “good enough” for a huge chunk of flows. plus L2s win on composability and distribution, and cheap high-throughput chains like pitch speed and cost for consumer-ish payments. So Plasma doesn’t get to show up and say “payments are big.” It has to answer “why would flows move here instead of staying where they already clear?” The only believable answer is a combo of cost, finality, and operational simplicity that’s meaningfully better for the specific job of stablecoin settlement.

What Actually Matters: Failure Rates, Confirmation UX, and “Pending Anxiety”

The part I’m watching, and the part the market tends to miss early, is that stablecoin settlement isn’t just “TPS,” it’s failure rates, reorg anxiety, confirmation UX, and how often you force a user to do an extra step. Sub-second finality is not a flex for Twitter, it’s the difference between a merchant treating funds as received versus pending. Gasless transfers are not charity, they’re customer acquisition. And EVM compatibility is not a checkbox, it’s how you reduce the integration time for wallets and payment apps that already have battle-tested codepaths. Plasma is basically saying: we’ll take the most common stablecoin actions and make them feel like sending a message, not like using a chain.

Risks: Value Capture, Distribution, and the Regulatory Spotlight

But you shouldn’t gloss over the risks, because the risks are exactly where “stablecoin-first” can backfire. First, if you make the default path gasless and stablecoin-denominated, you’re implicitly making the native token’s value capture less obvious. That can work if XPL is primarily a security asset and the chain becomes important enough that people want to stake and govern it, but it’s not automatic. Second, distribution is everything. If major wallets and payment front ends don’t route to you, your better design doesn’t matter. Third, any stablecoin-centric chain lives under a brighter regulatory lamp. The minute you matter, you’re in the conversation that banks, regulators, and issuers are having about what stablecoins do to deposits and payments. putting a number like “hundreds of billions in deposit risk” on stablecoins is not a fun headline if your entire product is built around accelerating that trend.

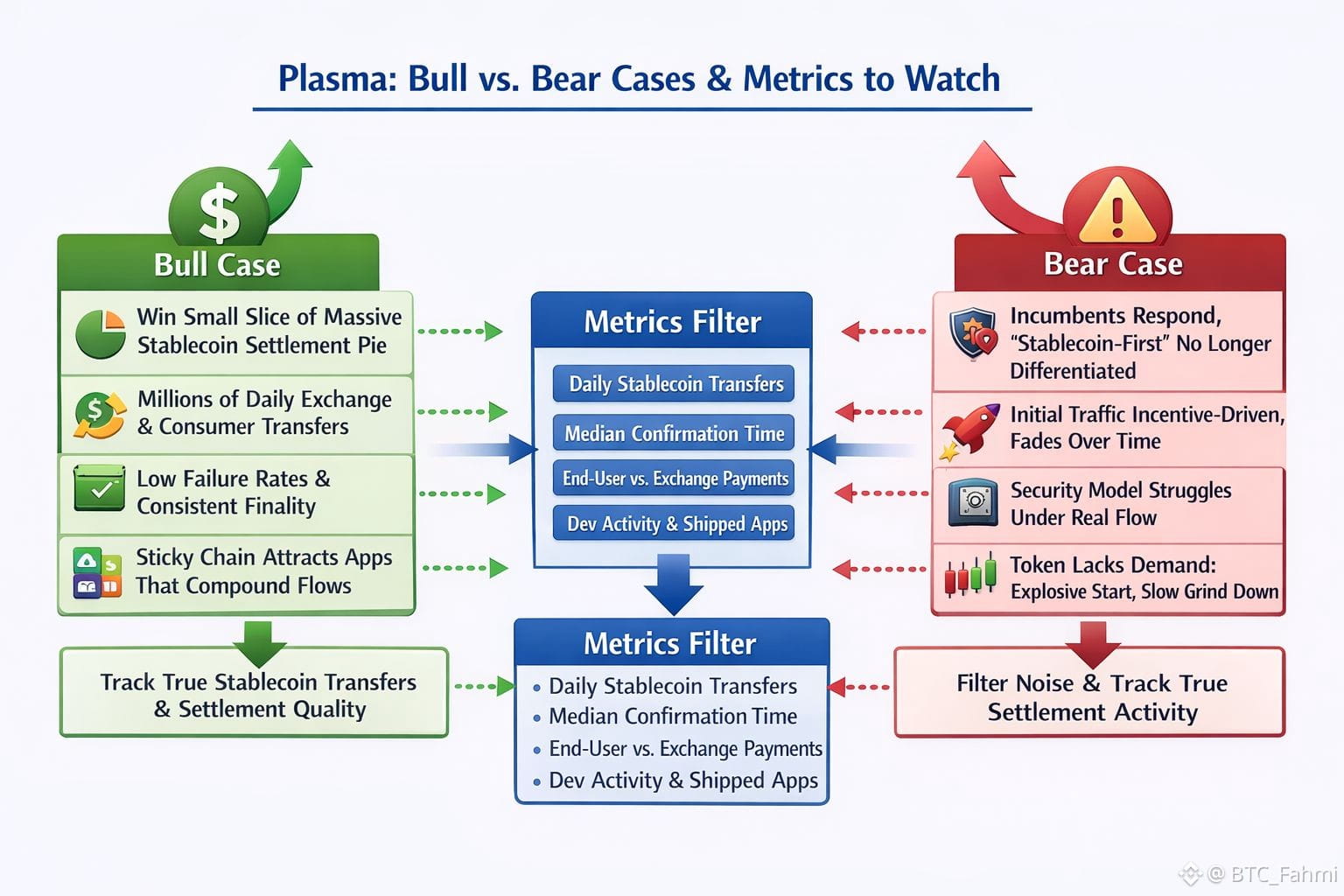

Bull Case: Win a Small Slice of a Massive Pie, Then Compound

So what’s the bull case that’s actually tradable, not just hopeful? It’s Plasma capturing a small slice of a very large pie in a way that compounds. If total stablecoin supply is roughly ~$300B and USDT is still the heavyweight, you don’t need Plasma to flip the world. You need it to become a meaningful settlement venue for a few high-frequency categories: exchange-to-exchange moves, merchant payment processors, remittance corridors, and wallet-to-wallet consumer transfers. If that translates into, say, millions of daily transfers with low failure rates and consistent finality, the chain becomes sticky. Once it’s sticky, app teams build on top of it because the money is already there, not because the tech is prettier.

Bear Case: Incumbents Respond + Incentive-Driven Activity Fades

And the bear case is straightforward. The incumbents respond. Fees compress everywhere. UX improves on existing rails. The “stablecoin-first” differentiator becomes table stakes, and Plasma is left fighting on marginal improvements while trying to prove its security model under real load. Or you get the classic early-L1 problem: activity shows up, but it’s incentive-driven and fades when emissions or campaigns roll off. In that scenario, $XPL trades like most new L1 tokens do: bursts on announcements, then a slow grind as the market demands proof in on-chain usage.

The Only Filter That Matters: Track Settlement Reality

My filter from here is simple. Don’t overthink the story, track the settlement reality. Daily stablecoin transfer count and volume on Plasma, median confirmation and finality UX in major wallets, the share of transfers that are true end-user payments versus exchange churn, and whether developer activity turns into shipped payment products rather than demos. If those lines slope up while the broader stablecoin market keeps expanding, Plasma has a real shot at becoming a default rail for certain flows. If they don’t, it’s just another token trying to out-market rails that already work.