While everyone is arguing about rate cuts, elections, and Bitcoin price targets, a far bigger problem is quietly ticking in the background.

A $9 trillion problem.

And almost no one is prepared for what happens next.

Between 2020 and 2022, the US government went on a historic borrowing spree. Trillions of dollars were issued at near-zero interest rates.

Free money. Cheap debt. No consequences. Or so it seemed.

Markets loved it. Stocks flew. Crypto exploded. Governments expanded spending like the bill would never come due.

Now fast-forward to 2026.

That debt doesn’t disappear.

It expires.

And it must be refinanced.

Here’s the catch:

Those near-zero rates are gone. Completely.

The US now has to roll that same debt at 5%+ interest rates instead of 0–1%.

Same principal.

Wildly different cost.

This is where the math breaks.

Why This Is a Disaster in Slow Motion

When rates were near zero, interest payments were manageable.

At 5%+, they explode.

Every percentage point increase adds hundreds of billions in annual interest costs.

That means more money spent servicing debt than on defense, infrastructure, or social programs.

The government didn’t just borrow cheap.

It locked itself into cheap forever.

And forever just ended.

The Four Ways Out (All Bad)

When this refinancing wall hits, there are only four possible outcomes:

1. Print massive amounts of money

This is the easiest option politically.

It also destroys the dollar’s purchasing power and reignites inflation.

2. Cut government spending

In theory, this fixes the math.

In reality, it’s political suicide. No administration survives it.

3. Raise taxes aggressively

This slows the economy, crushes consumption, and risks recession or worse.

4. Default or restructure

The nuclear option. Global confidence shock. Bond market chaos. Unthinkable… until it isn’t.

Notice the pattern?

There is no painless solution.

Every path leads to volatility, instability, or outright panic.

Why Markets Aren’t Pricing This In Yet

Because the crisis isn’t today.

It’s just far enough away to ignore.

Markets are short-term machines. Politicians are election-cycle thinkers.

The bill comes due after the headlines move on.

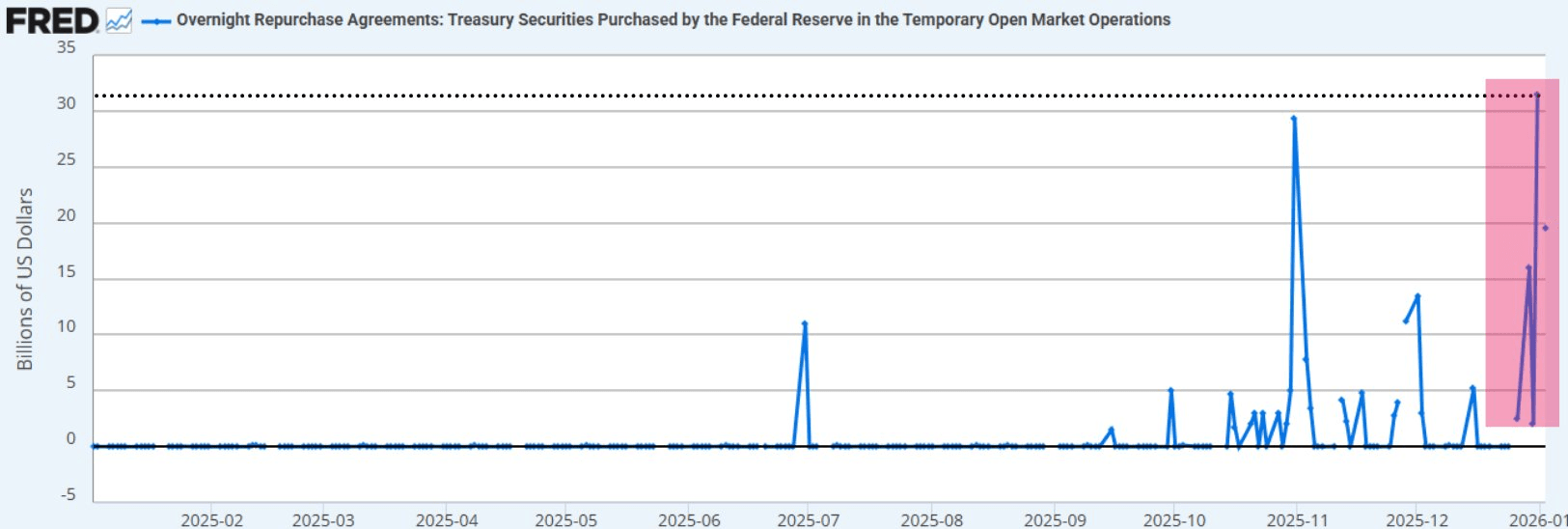

But when refinancing actually begins at scale, reality hits fast.

Bond yields spike.

Risk assets reprice.

Liquidity tightens.

And confidence cracks.

This is how “sudden” crises are born.