The divergence begins around 2009 the same period that marks the transition to a liquidity-driven global system.

Monetary structure changes first.

Asset repricing follows.

Let’s understand this shift in more detail.

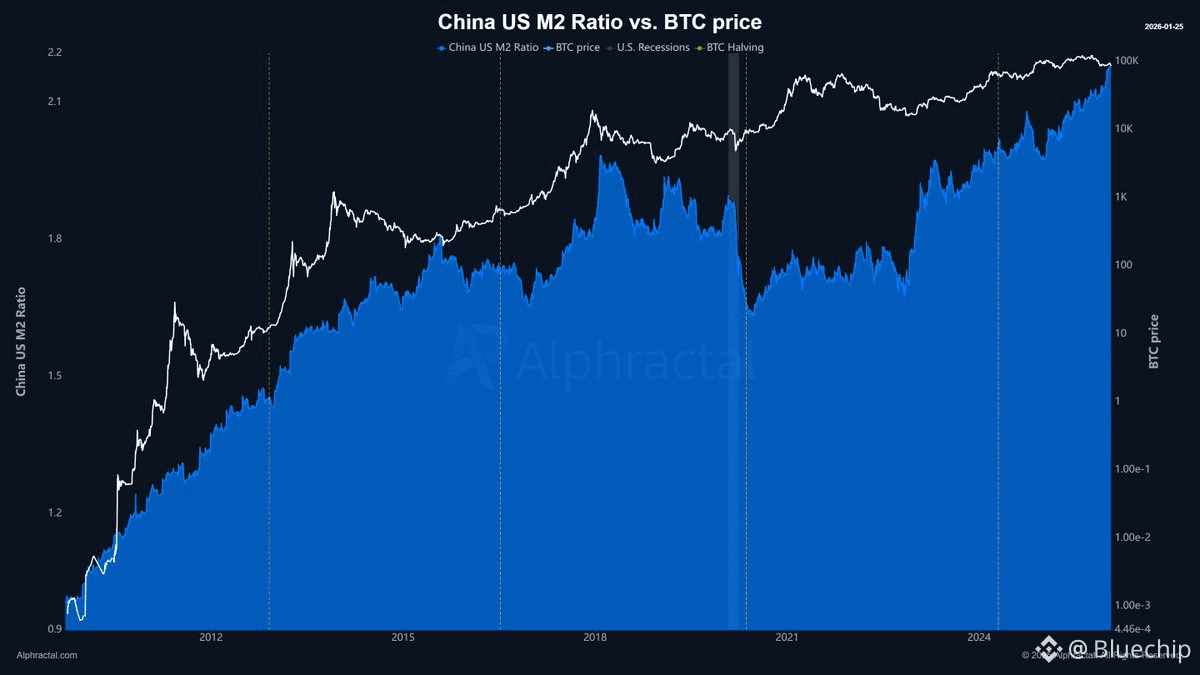

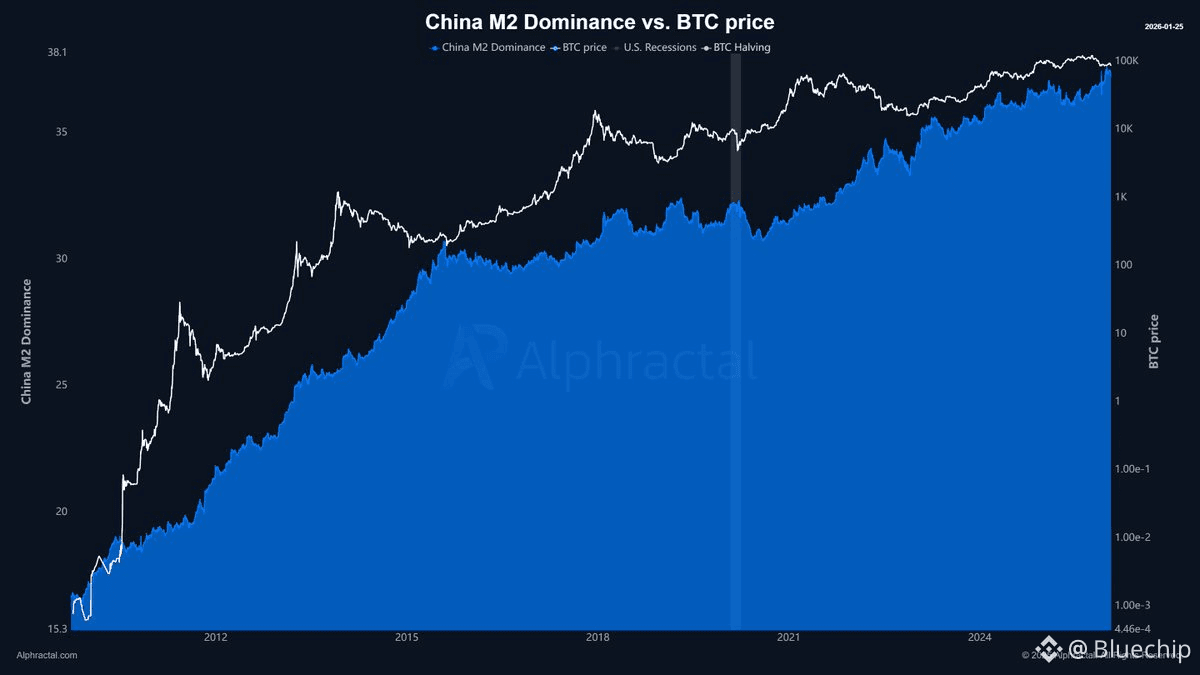

China’s growing dominance

China currently represents 37.2% of global M2 liquidity.

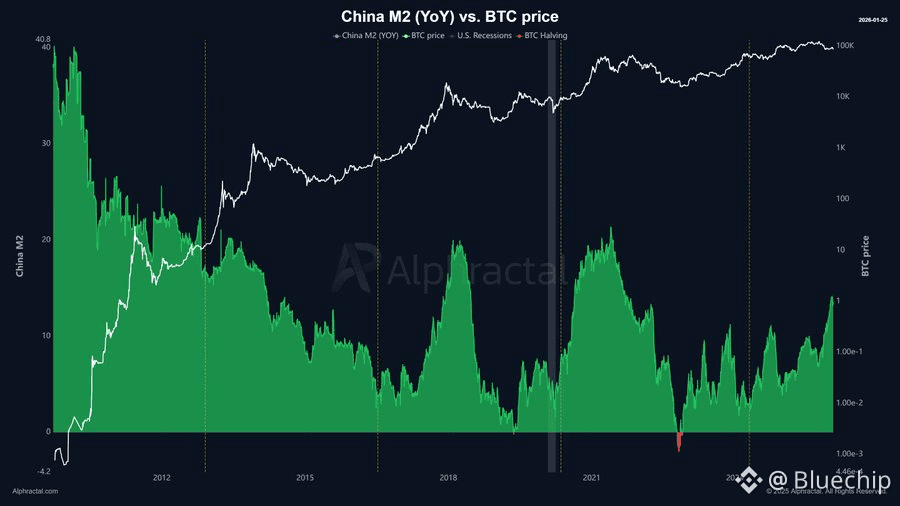

Since 2009, China has relied increasingly on credit expansion as a core policy tool, using its banking system to stabilize growth during downturns.

This dominance is not cyclical.

It is structural.

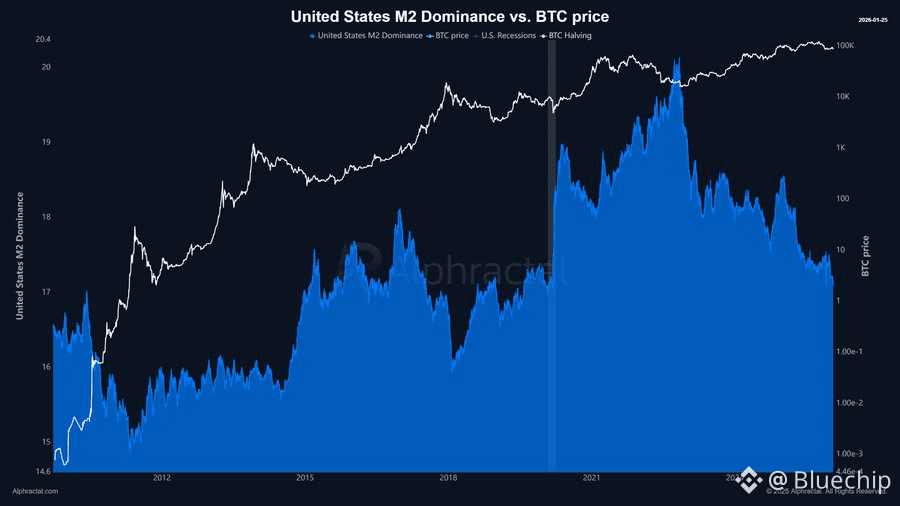

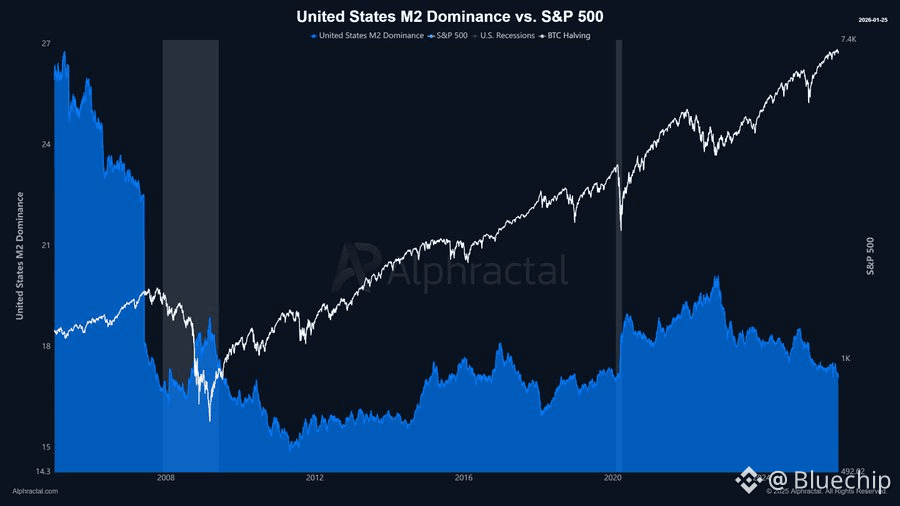

The declining U.S. share

The United States now accounts for only 17.1% of global M2.

For historical context:

In 2005, the U.S. held 26.4% of global monetary dominance.

The global liquidity center has gradually shifted east.

How China injects liquidity

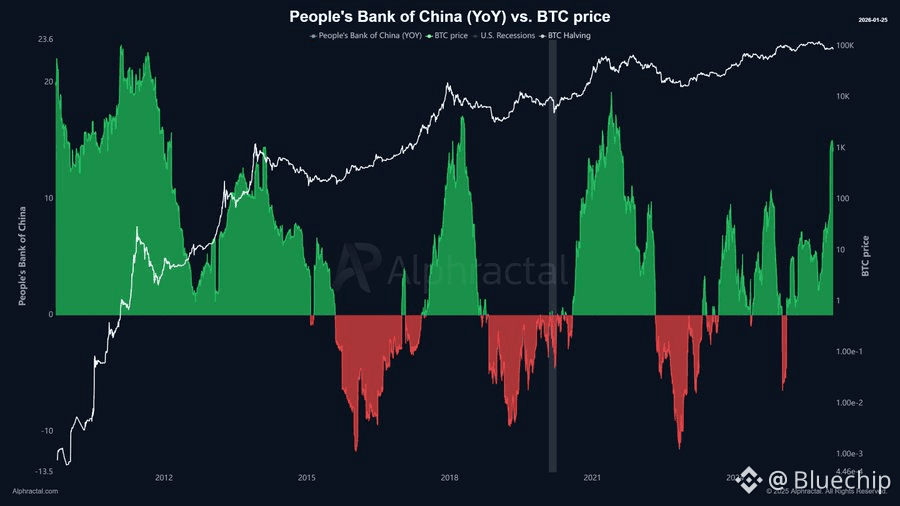

China’s monetary expansion occurs in credit waves, visible in the YoY changes of the People’s Bank of China.

Each acceleration phase reflects policy intervention aimed at offsetting economic slowdown, particularly in real estate and infrastructure.

Liquidity is deployed reactively but at scale.

Absolute scale matters

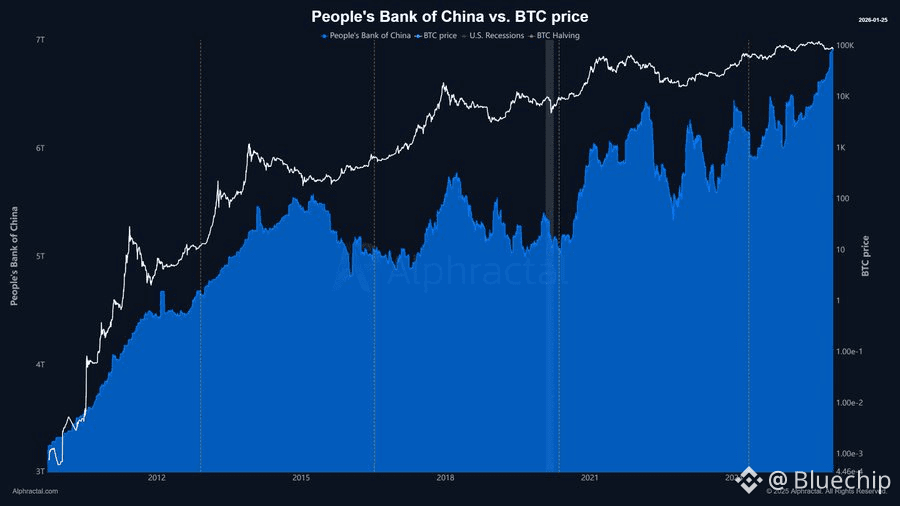

Central Bank balance sheet (China):

China’s central bank balance sheet expanded from roughly 3T to over 7T in just over a decade.

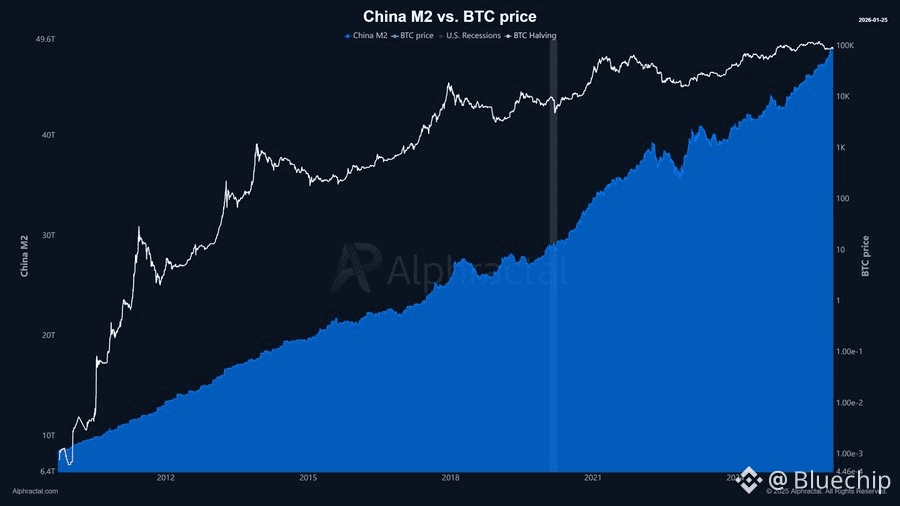

M2:

Over the same period, China’s M2 grew from approximately 10T to 49T.

This is not merely economic growth.

It reflects a system increasingly dependent on monetary expansion to maintain stability.

Liquidity is no longer a cycle.

It is the framework.

Why this matters

Since 2009, China has increasingly taken center stage in global liquidity creation.

The global monetary system has shifted from a U.S.-centric model to a liquidity-multipolar structure, with China emerging as the largest contributor by volume not through markets, but through sustained credit expansion.

This shift is not ideological.

It is mechanical.

When growth slows, liquidity expansion becomes the primary policy response.

Understanding where liquidity is created, how it is transmitted, and which system ultimately absorbs it is essential to understanding future asset repricing.

Monetary structure moves first.

Markets adjust later.